We believe Protolabs and Xometry are the two behemoths in the digital manufacturing space, and offer the two best on-demand manufacturing marketplaces.

Since March 1st, 2024, we have been uploading 3 different CNC part files and 3 different 3D printable files weekly to both Protolabs Network and Xometry to track pricing trends across the two marketplaces. By tracking prices on the same parts over time we believe we can gauge demand trends as prices should theoretically rise on these marketplaces as demand increases (assuming supply remains constant). In addition, we believe analyzing how each marketplace prices the same part can provide additional competitive insights. We focus on CNC and 3D printing prices as these services account for ~50% and ~75% of total sales for Protolabs and Xometry, respectively.

Historically our analysis as been a robust read-through into Xometry XMTR 0.00%↑ and Protolabs PRLB 0.00%↑ quarterly results. Below we highlight pricing trends through 4Q24, and provide implications to Xometry and Protolabs 4Q24 earnings results.

Key Pricing Takeaways: October, 1st 2024 - December 31st, 2024

Xometry US manufactured CNC prices consistently increased throughout 4Q24, with prices up ~8% on December 31st compared to the beginning of the quarter. However, international prices declined ~17% over this same time period.

Protolabs US manufactured CNC prices remained consistent through mid-December, but saw a modest uptick in the back-half of the quarter with prices up ~11% in the US on the last day of the quarter compared to the first. International pricing saw similar behavior with prices up ~6% over this time period.

Protolabs saw prices for 3D printed parts remain unchanged since we began tracking prices in 1Q24, while Xometry saw prices decrease in October, but returned to original pricing levels in mid-December.

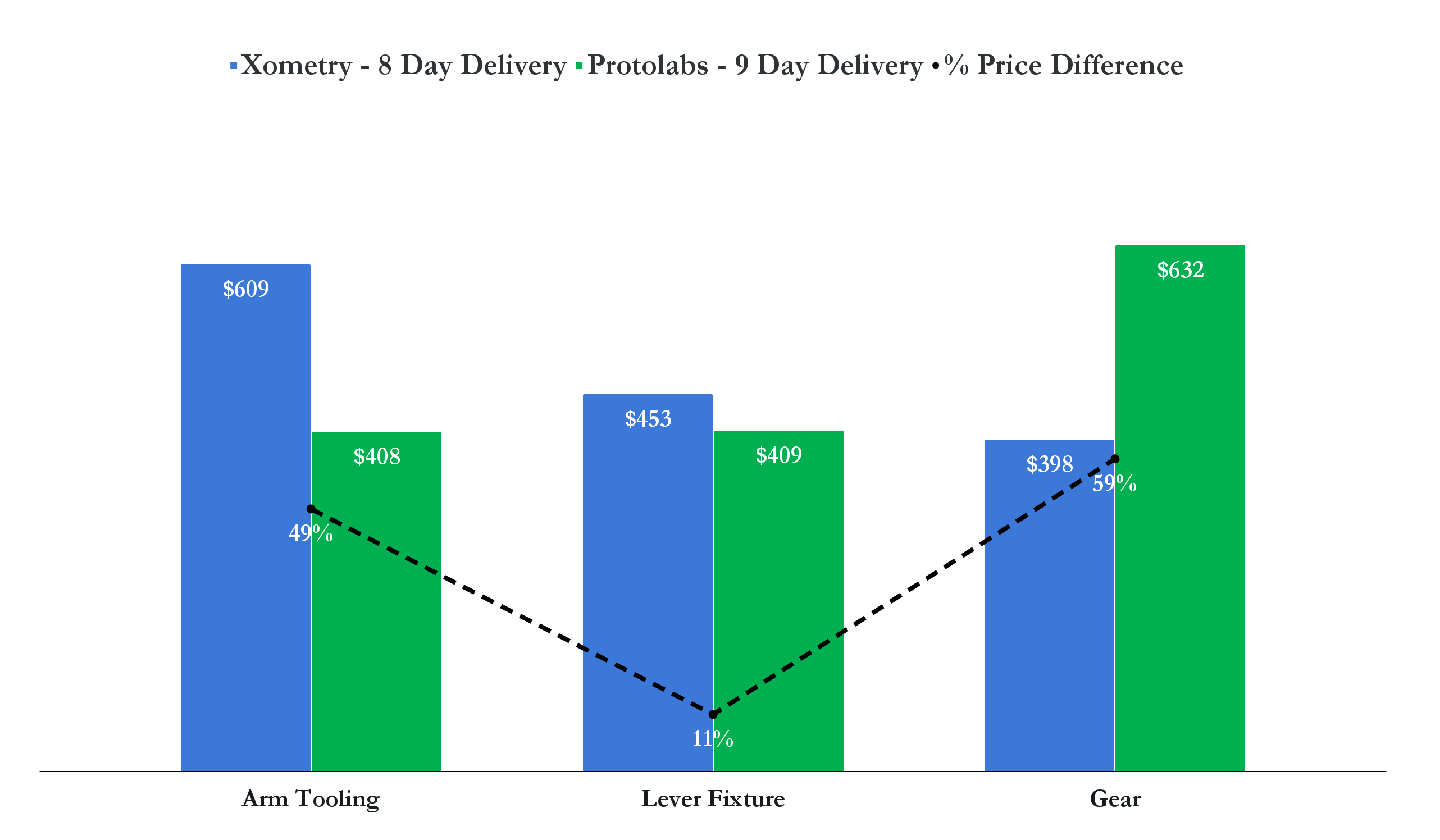

Protolabs on average was offering cheaper prices on 2 of 3 CNC parts manufactured in US and internationally compared to Xometry. Protolabs also offered lowered prices on all 3 3D printed parts compared to Xometry.

In mid-October Xometry lowered its delivery time from 10 to 8 days for US Economy pricing and 9 to 8 for International Economy pricing, which is what we use to track weekly pricing trends. Protolabs delivery days for their closest comparable shipping time is 9 in the US and 11 internationally.

Xometry and Protolabs international prices were 40-47% less expansive than producing the same CNC parts in the US.

ISM Manufacturing index was in contracting territory every month in 4Q24, but showed slowing declines in the back half of the quarter. We believe the improving ISM data, compliments our pricing analysis that suggests demand in the US improved across Protolabs and Xometry marketplaces in the back half of the quarter.

CNC US-Based Manufactured Price Analysis

Analysis based on total price basket of 3 aluminum parts to be produced via CNC by US-based manufacturers and delivered in a 8 - 11 day delivery window. Price Index consists of a base price of $100 on March 4th, 2024. A deviation up or down from $100 will indicate percentage change in price from the original basket of 3 parts on March 4th. For example, $107 implies the basket price for these 3 parts are 7% higher than they were on March 4th.

CNC US Manufactured Price Index

As shown below, Xometry US manufactured CNC prices consistently increased throughout 4Q24, with prices up ~8% on December 31st globally compared to the beginning of the quarter.

Protolabs US manufactured CNC prices remained consistent through mid-December, but saw a modest uptick in the back-half of the quarter with prices up ~11% in the US on the last day of the quarter compared to the first.

In mid-October Xometry, lowered its delivery time from 10 to 8 days for US Economy pricing, while Protolabs delivery days for their closest comparable shipping time is 9 in the US and has remained unchanged since tracking pricing.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

Average Weekly Part Price Trends (03.04.24 - 12.31.24)

As shown below, driven by Xometry’s price increase, Protolabs continues to offer lower prices on 2 of the 3 US manufactured CNC parts. However, Xometry now offers shipping 1 day faster than Protolabs on its most comparable price offering.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

Investor Gifts

Looking to become a better investor or need to find that perfect gift for your finance friend? Check out products from our partner at Investor Gifts, such as their 2025 Investor Calendar.

CNC International-Based Manufactured Price Analysis

Analysis based on total price basket of 3 aluminum parts to be produced via CNC by international-based manufacturers and delivered in a 9 - 11 day delivery window. Price index consists of a base price of $100 on March 4th, 2024. A deviation up or down from $100 will indicate percentage change in price from the original basket of 3 parts on March 4th. For example, $107 implies the basket price for these 3 parts are 7% higher than they were on March 4th.

CNC International Manufactured Price Index

As shown below, Xometry international CNC prices consistently decreased throughout 4Q24 with our average basket of parts pricing down ~17% at the end of the quarter compared to the last day of 3Q24.

Protolabs international CNC prices remained mostly unchanged through mid-December, but did see a modest step-up in the back-half of the quarter ending ~6% higher. As shown below, Protolabs international pricing continues to climb since we began tracking pricing.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

Average Weekly Part Price Trends (03.04.24 - 12.31.24)

On average, Protolabs offered lowered prices on 2 of the 3 International manufactured CNC parts, but Xometry prices offer delivery 3 days faster.

Xometry and Protolabs international prices were 40 - 49% less expansive than producing the same CNC parts in the US.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

3D Printing Price Analysis

Analysis based on total price basket of 3 3D printed nylon parts to be produced via Select Laser Sintering (SLS) and delivered in a 5 day delivery window. Xometry and Protolabs only offer US-based 3D printing services.

3D Printing Price Index

As shown below, Protolabs saw prices for 3D printed parts remain unchanged since we began tracking prices in 1Q24.

Xometry saw prices decrease in October, but returned to original pricing levels in mid-December.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

Average Weekly Part Price Trends (03.04.24 - 12.31.24)

As shown below, Protolabs on average offered lowered prices on all 3 3D printed parts.

Source: Protolabs and Xometry Website, Industrial Tech Analyst

ISM Manufacturing Data Improved in 4Q24, But Remains In Contracting Territory

As shown below, ISM Manufacturing index was in contracting territory every month in 4Q24. However, the index indicated slower declines in the back half of the quarter with ISM Manufacturing Index of 46.5, 48.4 and 49.3 in October, November and December, respectively. We believe the improving ISM data, compliments our pricing analysis that suggests demand in the US improved across Protolabs and Xometry marketplaces in the back half of the quarter.

ISM Manufacturing PMI (>50 = Expansion, <50 = Contraction)

Source: FactSet

4Q24 Earnings Previews

Protolabs: Positioned to Meet Guidance, with Upside Potential at the High End

We expect Protolabs to report 4Q24 earnings sometime during late February or early March. Given pricing trends remained solid throughout 4Q24, we expect Protolabs to report 4Q24 results in-line with previous guidance. Protolabs guided Q4 revenues in the range of $115 - 123M, which implies ~5% Y/Y decline at the midpoint. We believe Protolabs ~11% US and ~6% international price accretion in December likely suggests improving demand and would not be surprised if Protolabs comes in at the high-end of their guidance range. We will wait to see if these stronger pricing trends continue into 1Q25, but if they do, we believe there is a chance Protolabs could guide above current Street expectations of $124.5M. That said, we have yet to see indicators of a broader improvement in the manufacturing environment with ISM manufacturing index remaining in contracting territory in December. We are cautiously optimistic manufacturing activity may improve in 2025 driven by a new Trump administration and lower interest rates. While we believe an improving manufacturing environment will be the strongest catalyst for PRLB shares, we do believe the stock can continue to go higher in 2025 driven by operational efficiencies and robust earnings / FCF growth.

Looking longer term, we believe the combination of Protolabs Factory and Network business positions the Company as a clear leader in the digital manufacturing space. We expect the combination will allow Protolabs to acquire new customers, and more importantly grow wallet share per customer. We believe Protolabs will continue to grow and produce strong free cash flow, especially when the manufacturing market becomes more favorable. In turn, we reiterate our buy rating and $60.05 price target.

Link to our latest Protolabs model and reports.

Source: Industrial Tech Analyst

Xometry: Robust US Demand Overshadowed by Weak International Trends, Guidance at Risk

We expect Xometry to report 4Q24 earnings sometime during late February or early March. While Xometry US pricing trends are encouraging, we believe the ~17% decline in international prices is a cause for concern. Xometry guided 4Q24 revenues in the range of $145 - 147M, which implies ~14% Y/Y growth and up ~3% Q/Q at the midpoint. Given ~83% of sales comes from the US, we believe Xometry may still hit their original guidance, but we believe poor international pricing trends suggests sluggish international demand and could lead to a revenue miss. Furthermore, if international pricing doesn’t improve and/or US pricing doesn’t accelerate in 1Q25 we believe there is high risk the company could guide revenues below consensus estimates, which is currently calling for revenues of $151M or up ~23% Y/Y. That said, we believe investors focus will continue to shift towards profitability. The company guided adjusted EBITDA to be slightly profitable in 4Q24, but we believe the company could come in short of their forecast given the chance of sales coming in below expectations. Furthermore, recall on the company’s 3Q24 earnings call, they highlighted they expect revenues to accelerate in 2025, and expect to be adjusted EBITDA positive for the full year. Given these pricing trends we believe there is high risk the company guides down these expectations, which would be catastrophic to the stock and their credibility.

Xometry has been on a remarkable run, surging over ~230% in 2H24 as investors grow increasingly bullish on the name. This momentum follows two notable sell-side buy upgrades in December, further fueling the stock's ascent. While we are impressed by the company’s ability to grow in a recessionary manufacturing environment, which is likely a key driver of investor enthusiasm about its potential performance in a growing manufacturing environment, we remain cautious. We believe Xometry is a great tool to secure prototypes and low-volume production parts, but our bearish thesis is driven on the assumption Xometry will struggle to increase wallet share among customers, which we believe is a critical benchmark to grow adjusted EBITDA margins. As customers ramp up production, we believe they will go directly to the manufacturer, which is why we believe Protolabs is much better positioned. Driven by sluggish revenue per customer growth and expectation of higher opex spend to acquire new users in order to grow, we believe the company will continue to underwhelm investors profitability expectations. With the stock trading at a staggering 190x EV/EBITDA based on 2025 estimates, we remain unconvinced about Xometry’s ability to translate this growth into current elevated profitability expectations. In turn, we reiterate our sell rating and $9.40 price target.

Link to our latest Xometry model and reports.

Source: Industrial Tech Analyst

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.