Cognex Returns To Organic Growth In Q3 Coupled With Better Than Expected Profitability and Cash Flow

Key Takeaways: Cognex CGNX 0.00%↑ reported mixed 3Q24 results with revenues in-line with Management expectations and analyst estimates, as well as strong cost controls drove better than expected adjusted EBITDA and FCF. However, a continued more challenging macro backdrop resulted in 3Q24 guidance coming in slightly below analyst expectations. That said, the 3Q24 guide seems to be better than feared, and coupled with robust cost controls that led to strong free cash flow generation shares traded up 2-5% on these results.

Despite persistent macro headwinds across their factory automation businesses (specifically Automotive), we were pleased to see the company return to positive organic revenue growth (~7%). Furthermore, we believe Managements upbeat tone around logistics and growing opportunity around AI markets, as well as AI applications keeps our long-term bullish thesis intact. Machine vision is a critical getaway that blends the physical world with software, and we believe the rise of AI within manufacturing and distribution environments will directly grow demand for intelligent vision systems globally. We also believe AI will drive adoption across next gen consumer electronic devices, automotive vehicles and semis, which we anticipate will lead to capacity expansion across Cognex’s key verticals in the coming years. Coupled with the ability to generate strong earnings and cash flow in softer macro conditions, we see meaningful upside potential for “patient” long-term investors once manufacturing conditions improve. In turn, we reiterate our buy rating and price target of $64.14.

View detailed historical results in our full financial model here.

Source: Company Filings, FactSet; Data In Millions

Investor Gifts

Looking to become a better investor or need to find that perfect gift for your finance friend? Check out these products from our partner Investor Gifts like their 2025 Investor Calendar.

✓ US Economic Release Dates

✓ Option Expiration Dates

✓ Market Holidays

✓ Historical Market Returns

SAVE 20% with our exclusive promo SAVE20 at checkout!

3Q24 Earnings Summary

Cognex reported 3Q24 revenues of $234.7M, which was up 19.0% Y/Y and in-line with Management's previous guidance range ($225 - 240M) and consensus expectations ($233.4M). When excluding revenues from Mortiex, sales were up ~7% organically, which marks the first organic revenue growth in over 6 quarters. Sales in the quarter were led by continued strong momentum in logistics, as well as Semis and consumer electronics. However, auto and packaging all declined in the quarter. Auto continues to suffer from delayed and canceled projects in EV, as well as poor demand from traditional auto. The company expects these challenges to remain into 2025. Furthermore, Management seems upbeat about the opportunity in consumer electronics, and the expected upgrade cycle for new AI smartphone devices (Apple ~10% customer), but uncertainty remains on when those projects will accelerate. Lastly, Cognex continues to invest in a new GTM strategy, called Emerging Customer Initiative that is focused on expanding salesforce to reach under-penetrated customers. Cognex remains on plan to achieve their 2024 goals in this new initiative which includes, 80,000 customer visits, add ~3k new customers and target >75% grows margin. We believe the simplicity of new products driven by edge learning AI will allow the Company to serve new customers.

Non-GAAP gross margins in 3Q24 were 68.7%, which were down 370 basis points driven by the recent Moritex acquisition. Cognex showed strong cost controls in the quarter, with opex down Q/Q. This translated into adjusted EBITDA margins of 23.3%. The Company also generated strong cash flow, earning $56.3M in cash from operations and $51.9M in free cash flow in the quarter, which beat consensus FCF estimate of $40.2M.

Looking ahead, Management expects macro challenges to persist into 4Q24. In turn, Cognex provided revenue guidance in the range of $210 - 230M, which implies ~12% Y/Y growth at the midpoint but slightly missed consensus expectations of $223.2M. Non-GAAP gross margin is expected to be high 60s. Lastly, Cognex expects adjusted EBITDA to be in the range of 14 - 17% in 3Q24. Note Cognex does not include stock-based comp (SBC) in their EBITDA calculation.

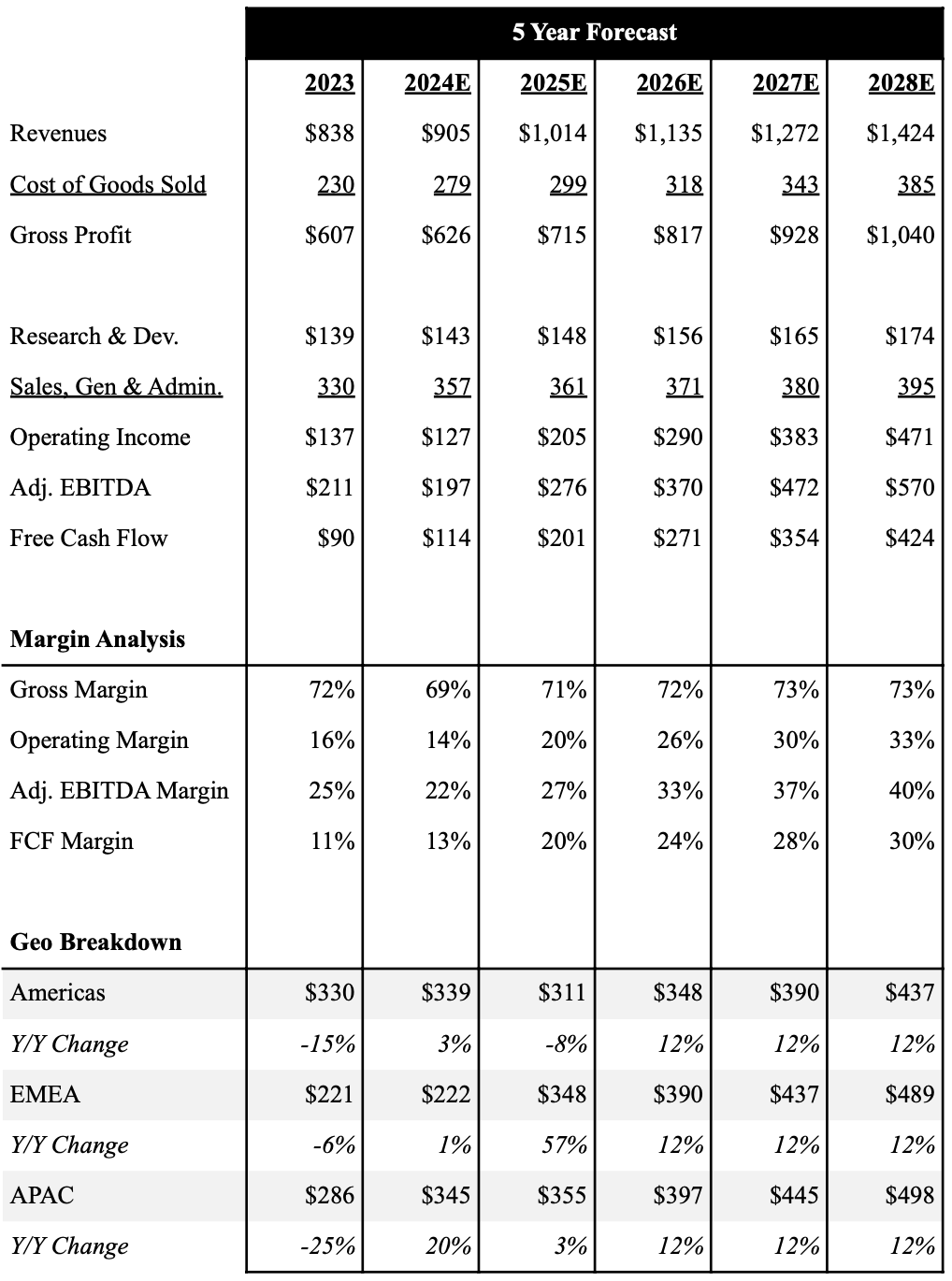

5-Year Financial Outlook

Following 3Q24 results, we believe most of our thesis remains intact, and have left our estimates mostly unchanged. We expect 2024 revenues to be up 8.1% Y/Y to $905.1M. Looking ahead, we expect the Company to see growth accelerate to 12.0% Y/Y in 2025, and sustain at least 12.0% revenue growth through 2028, which is-line with the machine vision industry.

As volumes increase in 2025 we expect the Company to sustain ~70.0%+ gross margins through 2028. We expect Cognex to continue to invest in R&D at a similar rate, and account for mid-teen percent of total revenues annually over the next 5 years. We are upbeat about Cognex’s Emerging Customer Initiative, and expect the Company to see material leverage as sales accelerate. Given the increased Sales & Marketing spend, we expect the Company to report Non-GAAP operating margins of 14.0% in 2024, which is still below their long-term target of ~30.0%. However, we believe Cognex will see more meaningful leverage return in 2025 as these investments slow, and see non-GAAP operating margins exceed 20.0% in 2025. We expect Cognex to see additional leverage in the years to come and reach their 30.0% operating margin target in 2027. Cognex has historically reported EBITDA margins of ~30.0%, but keep in mind the company does not include stock-based comp (SBC) in their EBITDA calculation. When including SBC, adjusted EBITDA margins have been north of 35%. We include SBC in our adjusted EBITDA calculation, and expect the Company to see adjusted EBITDA grow from $207M in 2024 to over $575M by 2028. We expect strong adjusted EBITDA growth to translate into robust free cash flow, with FCF margins consistently exceeding 20%+ starting in 2025 through 2028.

Below is an overview of our 5 year outlook with a full downloadable financial model here.

Source: Industrial Tech Analyst, Data In Millions

Investment Thesis

We view Cognex as a leading provider of machine vision and key enabler of factory and warehouse automation. Machine vision is a critical getaway that blends the physical world with software, and we believe the rise of AI within manufacturing and distribution environments will directly grow demand for intelligent vision systems globally. We also believe AI will drive adoption across next gen consumer electronic devices, automotive vehicles and semis, which we anticipate will lead to capacity expansion across Cognex’s key verticals in the coming years. We are also upbeat about Cognex's Emerging Customer Initiative, which we believe will drive adoption among many companies who have yet to fully utilize automation. Driven by an AI revolution, we believe the Company is positioned to see 12%+ revenue growth over the next couple years. Coupled with industry leading gross margins (~70%) and a scalable operating model, we anticipate accelerating revenue growth will translate into 35%+ earnings growth. These all support our bullish stance, which drives our price target of $64.14 and equates to 50%+ upside.

As shown in our table below we use a 5 year DCF model to value Cognex shares. Based on our current forecast that includes an average 30x EBITDA multiple to our terminal value, we value Cognex shares at $64.14.

Source: Industrial Tech Analyst, Data In Millions Except Price Target

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.