Initiation Report: Cognex, A Gatekeeper For AI Adoption On The Factory Floor and Warehouse - BUY

Initiation Report: Cognex, A Gatekeeper For AI Adoption On The Factory Floor and Warehouse - BUY

Company Overview - Cognex CGNX 0.00%↑ is a global provider of machine vision products and software solutions that automate the manufacturing and distribution of discrete items, by locating, identifying, inspecting, and measuring them across attractive industrial end markets. Cognex sells to customers in nearly all industries in which discrete items are manufactured on an assembly line or moved through a distribution center. Their largest industries by revenue are the automotive, logistics, and consumer electronics industries, which combined represented ~65% of our total revenue in 2023. From a customer concentration perspective, we believe within the consumer electronics vertical Apple accounts for ~10% of total sales, while Amazon is their largest logistics customer accounting for another ~10% of sales. Cognex is traded on the NASDAQ exchange under the ticker CGNX, and is headquartered in Massachusetts.

Investment Thesis: We view Cognex as a leading provider of machine vision and key enabler of factory and warehouse automation. Machine vision is a critical getaway that blends the physical world with software, and we believe the rise of AI within manufacturing and distribution environments will directly grow demand for intelligent vision systems globally. We also believe AI will drive adoption across next gen consumer electronic devices, automotive vehicles and semis, which we anticipate will lead to capacity expansion across Cognex’s key verticals in the coming years. We are also upbeat about Cognex's Emerging Customer Initiative, which we believe will drive adoption among many companies who have yet to fully utilize automation. Driven by an AI revolution, we believe the Company is positioned to see 15%+ revenue growth over the next couple years. Coupled with industry leading gross margins (~70%) and a scalable operating model, we anticipate accelerating revenue growth will translate into 35%+ earnings growth. These all support our bullish stance, which drives our price target of $67.36 and equates to 40%+ upside.

Robust Demand Driven By AI Revolution: Driven by challenging end-market demand in key verticals, as well as absorption of excess capacity built post pandemic among key logistic customers, Cognex saw revenues decline ~17% in 2023. While revenues across most of their factory automation end markets were down Y/Y in the 1Q24, Management indicated they are seeing early indications of recovery in certain end markets. Specifically, logistics and semis were up 24% and 6% Y/Y, respectively on an organic basis. Given the manufacturing environment remains challenging in most geographies, we believe growth may be sluggish near term. However, we believe growth can accelerate in 2H24 and continue into 2025 as AI drives increasing automation in factories and warehouses globally. Furthermore, we anticipate demand for AI enabled next gen consumer electronics and automotive vehicles drives meaningful capacity expansion initiatives. For example, Apple (~10% customer), is planning its first big AI rollout in smartphones this Fall and consumers will need the iPhone 15 Max or newer version to access many of these features. Given we estimate ~10% of Apple’s iPhone base will not have access to these features, we believe it sets up a meaningful upgrade cycle over the coming years.

Scalable Operating Model To Drive 35%+ Earnings Growth: Although the machine vision competitive landscape has intensified over the years, Cognex has sustained industry leading gross margins. Since 2019, Cognex Non-GAAP gross margins have ranged from 72.0 - 74.5%. Although we expect the competitive landscape to persist and possibly intensify, we believe Cognex’s technology leadership will allow them to maintain 72%+ gross margins. Cognex’s technology leadership is driven by the Company’s internal R&D efforts, which has accounted for mid-teens percentage of total sales. Cognex’s go-to-market (GTM) strategy is led by a direct sales force, which accounts for 70% of sales, as well as a partner led strategy accounting for the remaining 30%. The Company is investing in a new GTM strategy, called Emerging Customer Initiative that is focused on expanding salesforce to reach underpenetrated customers. Cognex believes the simplicity of new products driven by edge learning AI will allow the Company to serve new customers. This initiative will lead to ~$25M in opex increase in 2024, but drive ~$50M in revenues. This initiative is expected to be gross margin accretive immediately and in line with their 30%+ adjusted operating margin target over the long-term. Increased GTM expenses, coupled with declining revenues, has depressed operating margins to mid-teens in 2023, which is below historical levels that ranged from 25% - 30%. Historically, when Cognex has been able to grow revenue double-digits this has translated into robust operating leverage and operating income growth of 40%+. While higher sales investments near term may hinder profitable growth rates, we expect the acceleration in demand will drive at least 35%+ operating and net income growth over the next couple years.

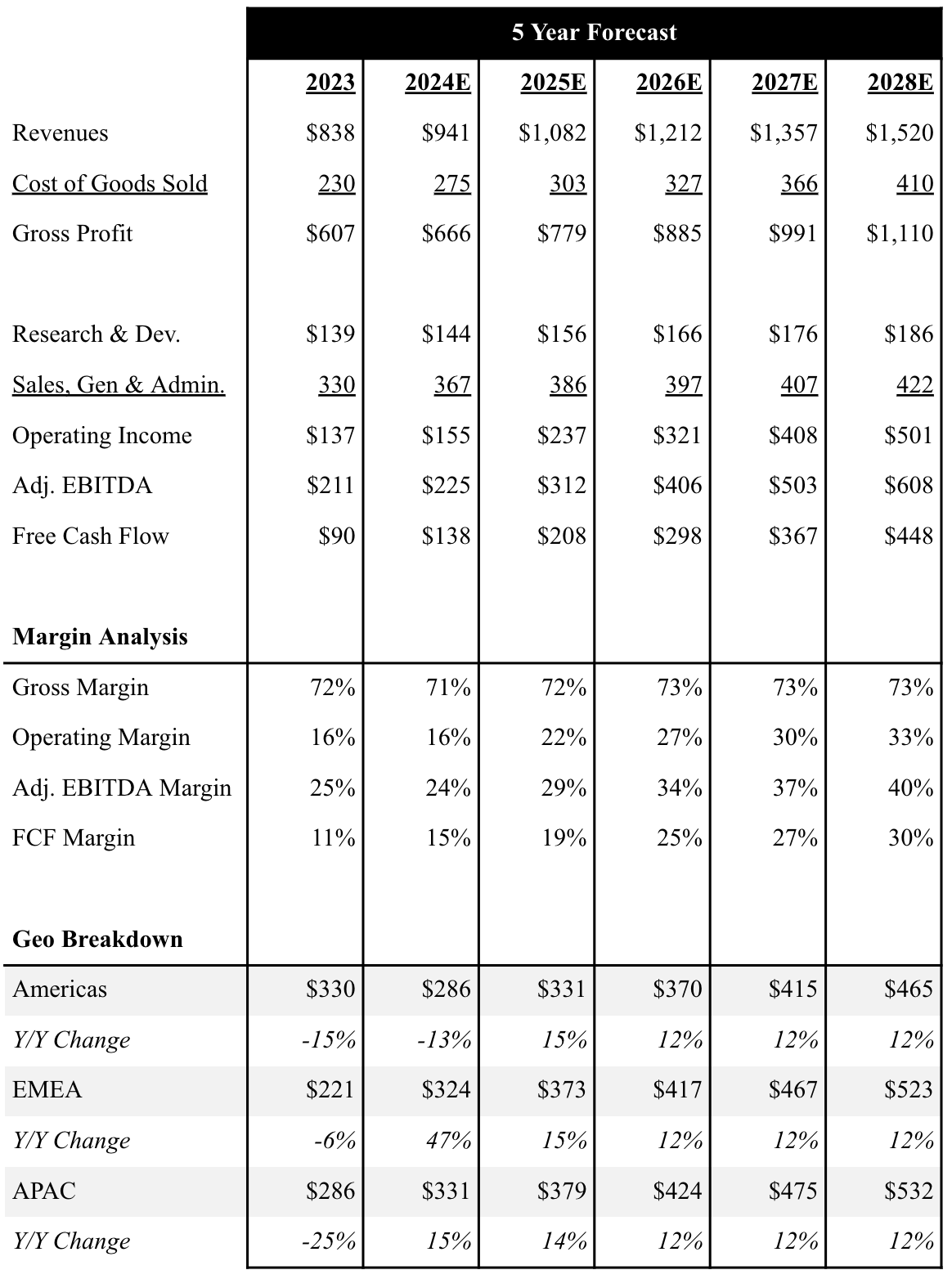

Financial Outlook: Cognex provides quarterly revenue, gross margin and opex guidance, but does not provide annual guidance. On the Company’s 1Q24 earnings call, Cognex guided 2Q24 revenues of $230 - 245M, which implies ~12.0% growth sequentially but down ~2.0% Y/Y. Although we anticipate the macro environment will remain challenging throughout 2024, we believe Cognex will see demand improve in 2H24 led by improving demand from logistic customers, as well as other verticals led by increasing AI adoption on the factory floor and distribution centers. We currently expect 2H24 revenues to be up 25% Y/Y, which will translate into revenues growing 12.3% in 2024 to $940.8M, which is modestly higher than consensus expectations of $933.1M. Looking ahead, we expect the Company to see growth accelerate to 15.0% Y/Y in 2025, and sustain at least 12.0% revenue growth through 2028, which is-line with the machine vision industry.

As highlighted previously, we expect the Company to sustain ~72.0%+ gross margins through 2028. We expect Cognex to continue to invest in R&D at a similar rate, and account for mid-teen percent of total revenues annually over the next 5 years. We are upbeat about Cognex’s Emerging Customer Initiative, and expect the Company to see material leverage as sales accelerate. Given the increased Sales & Marketing spend, we expect the Company to report Non-GAAP operating margins of 16.4% in 2024, which is still below their long-term target of ~30.0%. However, we believe Cognex will see more meaningful leverage return in 2025 as these investments slow, and see non-GAAP operating margins exceed 21.0% in 2025. We expect Cognex to see additional leverage in the years to come and reach their 30.0% operating margin target in 2027. Cognex has historically reported EBITDA margins of ~30.0%, but keep in mind the company does not include stock-based comp (SBC) in their EBITDA calculation. When including SBC, adjusted EBITDA margins have been north of 35%. We include SBC in our adjusted EBITDA calculation, and expect the Company to see adjusted EBITDA grow from $224M in 2024 to over $600M by 2028. We expect strong adjusted EBITDA growth to translate into robust free cash flow, with FCF margins consistently exceeding 20%+ through 2028.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Valuation: Driven by Cognex industry leading margin profile, the Company has historically traded at a premium valuation to our industrial comp group. Cognex is currently trading at ~31x EV/EBITDA based on 2025 estimates, which is in-line with their 5-year FY2 average EV/EBITDA multiple and modestly above our industrial comp group average of ~25x. View comp table here. We believe as revenue growth accelerates and operating margins return to normalized levels, Cognex can see multiple expansion, which is common during growth cycles. Historically, Cognex can trade north of 40x EV/EBITDA during years of growth. Furthermore, we are extremely bullish on the AI revolution, which is still in the very early innings and believe there is a possibility of upward revisions to our estimates.

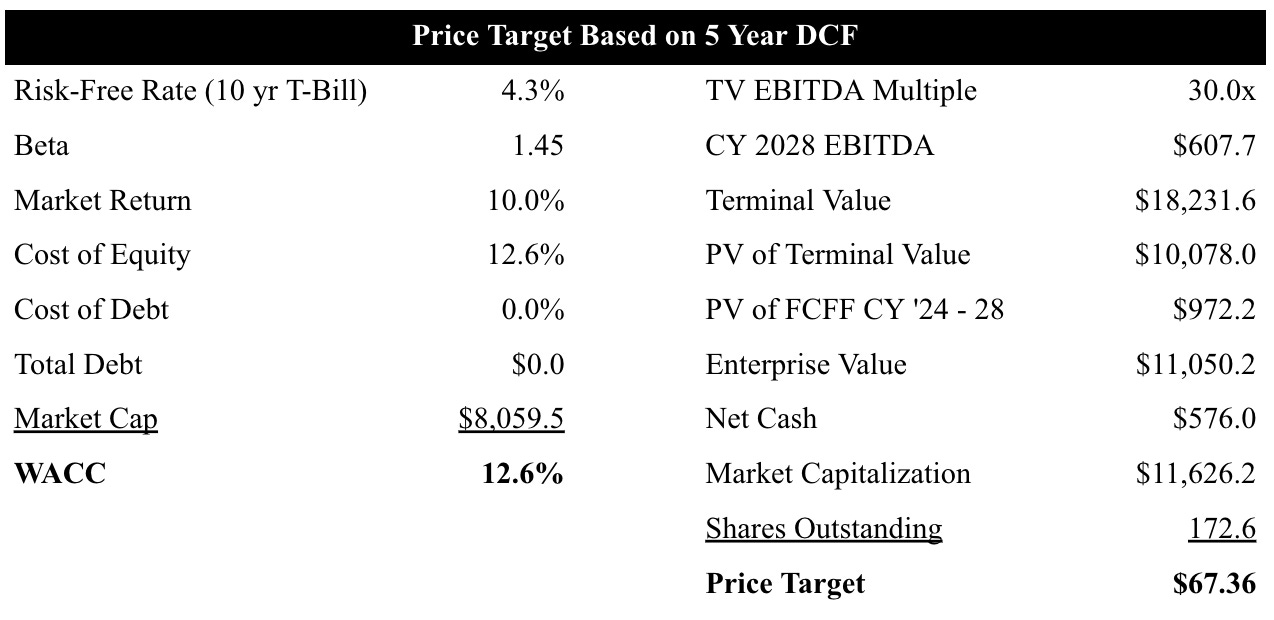

As shown in our table below we use a 5 year DCF model to value Cognex shares. Based on our current forecast that includes an average 30x EBITDA multiple to our terminal value, we value Cognex shares at $67.36, which equates to ~40%+ upside at current levels.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.