Initiation Report: Red Cat To Benefit From Global Drone Supercycle w/ Massive Near Term US Army Catalyst Opportunity - BUY

Initiation Report: Red Cat To Benefit From Global Drone Supercycle w/ Massive Near Term US Army Catalyst Opportunity - BUY

Company Overview

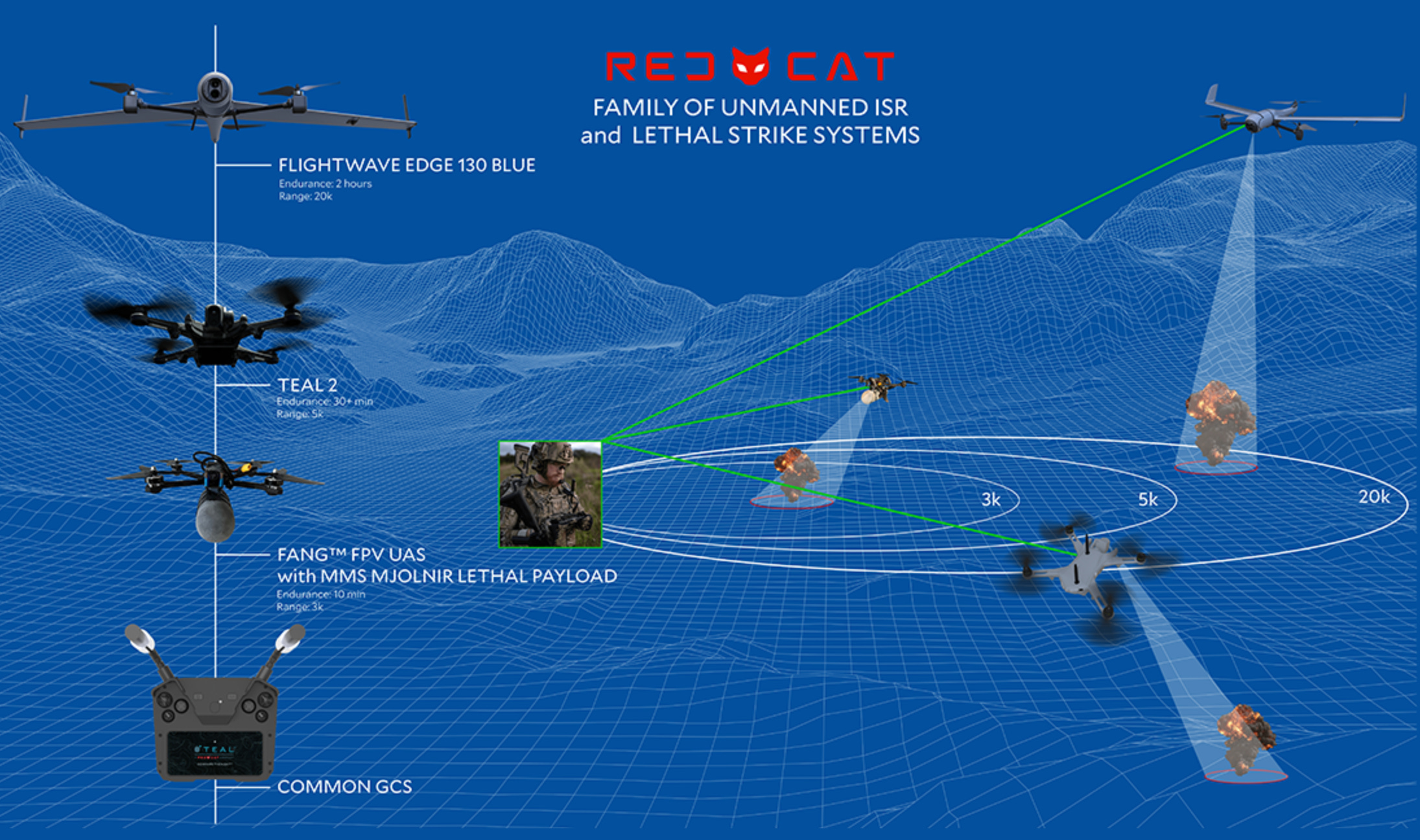

Red Cat Holdings RCAT 0.00%↑ is a U.S.-based technology company that designs, develops, and delivers cutting-edge drone solutions in defense applications. Red Cat flagship product, the Teal 2 drone, is a military-grade UAS designed for short-range reconnaissance missions. The Teal 2 is equipped with advanced features like night vision capabilities and secure communications, making it ideal for military and tactical operations. Red Cat also provides Edge 130 Blue through its recent acquisition of Flightwave, which is a Hybrid vertical takeoff and landing (VTOL) system, for long range reconnaissance missions with up to 2 hours of flight time. Lastly, their FANG solution is a first person view (FPV) drone with a flight time of 10 minutes with lethal surgical strike capabilities. The company is part of the U.S. Department of Defense's Blue sUAS program, which provides secure, American-made drones for defense use. Red Cat is also expanding its presence in global markets with their advanced drone technologies. The company is traded on the NASDAQ exchange under the ticker RCAT, and is headquartered in San Juan, Puerto Rico with a manufacturing facility in Utah.

Source: Red Cat Website

Investment Thesis

Red Cat is uniquely positioned to capitalize on what we believe is a global defense drone supercycle. Being a U.S.-based manufacturer and a participant in the U.S. Department of Defense's Blue sUAS program, we believe Red Cat stands to benefit meaningfully from favorable US legislation and the potential to be awarded material multi-year contracts from the DoD and international government agencies. If any of these programs are awarded, it creates a significant market opportunity providing the potential for $100M+ revenue streams per year and elevating Red Cats status as a leader in military drone technology. It would also materially impact the stock given Red Cat guided FY25 revenues in the range of $50-55M, which excluded any large defense programs. Specifically, the US Army is expected to announce the winner of the Short Range Reconnaissance (SRR) T2 program in the next few weeks, of which Red Cat was one of two finalists. That said, in the event Red Cat is not awarded any of these contracts near term, we believe Red Cat is still in position to see 30-50% annual revenue growth through 2028 driven by sustained traction they are seeing domestically across other government agencies, as well as internationally. While our biggest concern is the need to raise additional capital and historically defense spending can be hard to predict and lumpy, global defense spending on unmanned systems is only expected to grow around the globe. In turn, we believe Red Cat is poised for substantial upside driven by its strategic position in this global drone supercycle and we initiate coverage with a buy rating and $5.80 price target. Note if Red Cat is awarded the SRR, our price target is likely to go significantly higher.

Emerging Leader In Global Defense Drone Space - The drone industry is experiencing rapid growth across sectors like defense, infrastructure inspection, agriculture and logistics. Red Cat is well-positioned to benefit from this expanding demand, with a strategic focus on defense. As one of the few companies approved by the U.S. Department of Defense under the Blue sUAS certification, which are drones that have passed the Defense Innovation Unit evaluation, we believe Red Cat holds a competitive advantage in securing military contracts as defense budgets are increasingly prioritizing unmanned systems. Additionally, Red Cat’s growing credibility as a leading US drone company is helping expand into global markets, specifically NATO countries. We believe this further enhances its ability to capture market share in defense sectors worldwide.

Favorable Legislation To Benefit US Drone Companies - The American Security Drones Act and the Countering CCP Drones Act significantly benefit Red Cat by creating a regulatory environment that favors U.S.-based drone manufacturers over foreign competitors, particularly low-cost Chinese companies such as industry leader DJI. The American Security Drones Act, which was passed and included in the 2024 National Defense Authorization Act eliminates the use of drones by government agencies made by foreign companies. Furthermore, the Countering CCP Drones Act, which we believe will be signed into law as part of NDAA 2025, will regulate airwaves to ban foreign drones from using US controlled frequencies. This would essentially destroy foreign drones in US airspaces.

Massive Near Term US Army Program Catalyst - A program of record in the Department of Defense, is the holy grail among defense suppliers. It refers to a program that is included in the DoD's budget planning, with millions of dollars usually allocated for several years. We believe the U.S. Army’s Short Range Reconnaissance (SRR) is the first real chance the company is awarded a massive program of record. The SRR program aims to develop and procure small, portable drones for short-range reconnaissance missions. SRR is divided into two tiers T1 & T2. The T1 program is complete and includes just over ~1,000 drones. The program paid out ~$20m upfront and included additional purchases rising to $100m value over five years. T2 is estimated to demand 6x more drones, which could push the total contract value north of $500M over 5 years. Red Cat did not win T1, but their Teal 2 drone was not fully ready and the company likely lacked manufacturing capacity to meet the demand. Of the 37 original competitors for T2, Red Cat and Skydio remain the final 2 in contention for this program, which could be announced as soon as September. While Skydio did win a portion of T1, we believe Skydio’s drone failed to meet expectations in the field showing high rate of signal jamming, security concerns due to key components the drone leveraged and poor performance flying at night. We believe Red Cat’s Teal 2 aligns extremely well with the requirements of the SRR T2 program. On Red Cat’s 1FQ25 conference call, Management highlighted that the Army has declared a clear winner, but the companies have not been notified. Management expects an update during the first week of October or at the Army’s AUSA conference from October 14th - 16th. If awarded, the upfront payment of what we believe is $50M+ and $100M+ in annual orders, is significantly higher than the company's current annual run rate.

Other Massive Defense Contract Opportunities - In addition to the SRR program, we believe Red Cat has the opportunity for additional wins through the Pentagons Replicator initiative, which is focused on acquiring thousands of cheap, autonomous drones for multiple defense agencies. The Senate Appropriations Committee approved a defense spending bill for fiscal 2025 that would provide full funding for the Pentagon's Replicator Initiative. This DoD funding for drones is going to be the primary vehicle the US government uses to kick-start domestic production. This budget passed the continuing resolution last year and other allocations will result in about $1.5 billion in funds for Replicator alone going to drone manufacturers from now until September of 2025, which is approximately $100M per month. Lastly, the company is in contention to be awarded a program of record in NATO that is estimated to be 4x larger than the SSR program. Red Cat’s involvement in these large programs would signal to the broader market that its products meet stringent military standards, potentially leading to further defense contracts, both domestically and internationally.

Competitive Landscape

The competitive landscape for defense drones is very intense among established giants and emerging players globally. Red Cats closest competitors in the low-end intelligence, surveillance, and reconnaissance (ISR) drone space are Chinese based DJI, who has a global presence and Skydio, who is their biggest domestic competitor. AeroVironment, Lockheed Martin, and Northrop Grumman are less competitors in the low end drone markets, but do offer extensive portfolios of military-grade drones.

Investor Gifts

Looking to become a better investor or find that perfect gift for your finance friend?

Check out these products from our partner Investor Gifts.

Financial Outlook

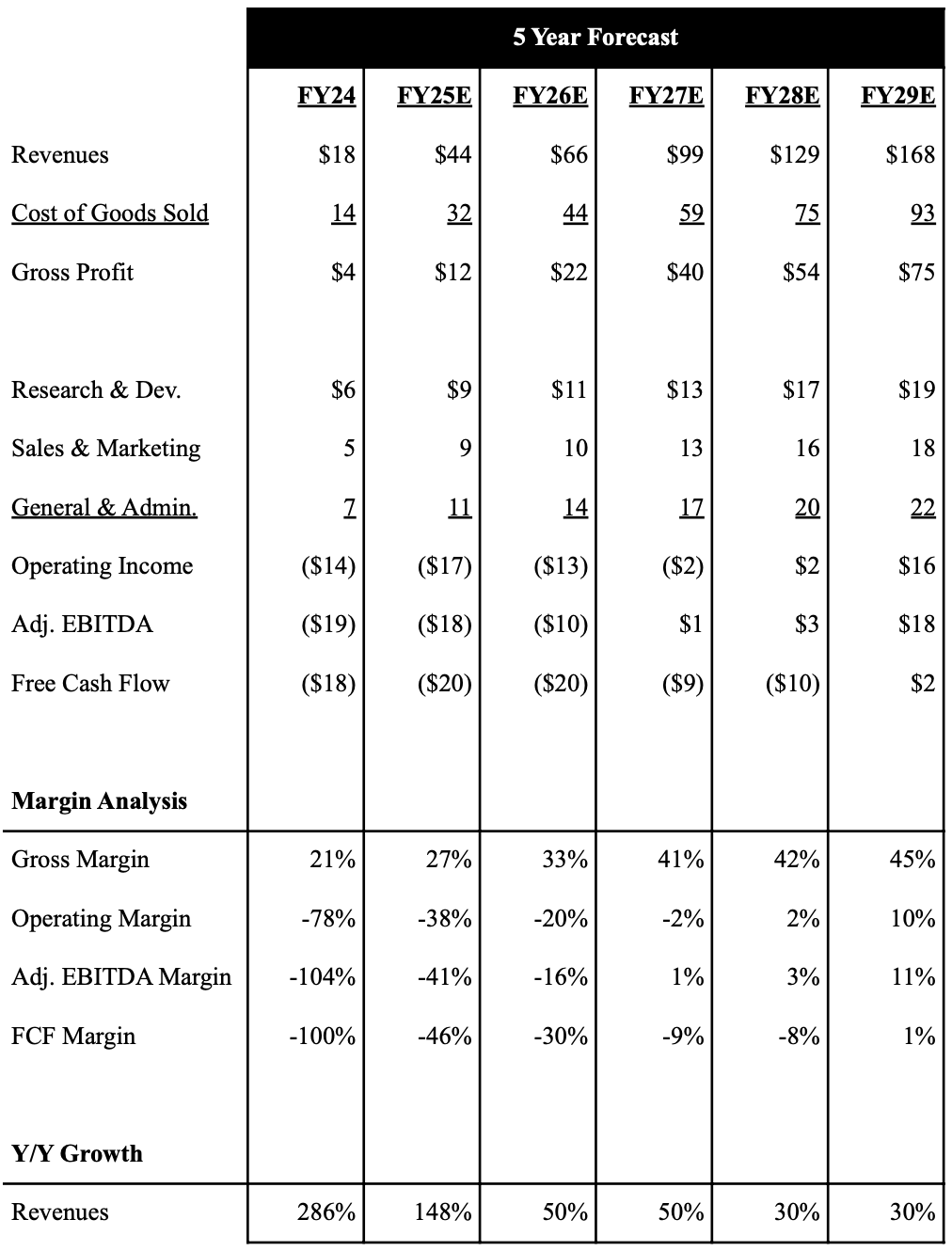

Red Cat is coming off its strongest ever fiscal year, with revenues growing 286% Y/Y to $17.3M. Revenues were driven mainly by the company’s newest product Teal 2, and did not include any revenues from any program of record production contracts. Looking ahead, the company recently guided FY25 revenues in the range of $50-55M, which represent 194% Y/Y growth at the midpoint and Management acknowledged this guidance excludes large DoD or NATO program contracts. Note heading into 1FQ25 earnings analysts were modeling FY25 revenues to be $32.6M! We believe the company will continue to see momentum domestically across multiple government agencies, as well internationally as geopolitical tensions remain elevated. In addition, the company is entering FY25 with a broader drone portfolio as the company will be shipping long range Edge 130 Blue systems with the acquisition closing in September. In fact, the company believes this system could generate $25M in revenues alone in FY25, but we believe it will take time to ramp. Coupled with the expectation defense sales could be impacted by timing delays, we are currently modeling revenues to grow slightly below company guidance to $44.2M, but sustain at 30-50% annual growth through FY29, exceeding $168M in revenues. We do believe sales may be lumpy on a quarterly basis given a growing percentage of their sales is contract revenues with government agencies that historically can be impacted by timing of funding. That said, we want to highlight that our estimates do not bake in any revenue from the possibility of being awarded the pending SSR T2 program or significant allocation of the Replicator initiative or NATO programs. If any of the three were awarded, we believe these programs could conservatively add $50M+ in annual revenues to our estimates.

As the company continues to ramp up production of their latest Teal 2 drone, gross margins have been lumpy but improved significantly in FY24 to 20.6%. As revenues grow, we expect gross margins to continue to expand annually, but expect quarterly gross margins to continue to be lumpy. We expect gross margins to reach mid-40% in FY29, but believe if the company secured any of the large outstanding DoD contracts gross margins could go materially higher driven by scale efficiencies. Given the high competitive pressure in the drone industry, Red Cat has needed to invest in R&D, Sales & Marketing and G&A to build out the necessary infrastructure of an emerging company. We do expect these operating expenditures to continue to grow as revenues scale up, but expect the company to see improving operating leverage each year. We currently expect the company to reach adjusted EBITDA positive in FY27, but like gross margins, this timeline could accelerate in the event they are awarded any large government contracts domestically or internationally. That said, the company is burning low-mid single digits a quarter in cash, and ended 1FQ25 with $7.7M in cash and cash equivalents. However, the company announced on their 1FQ25 earnings call they raised $8M in debt at the end of September, which will last them through January/February at which time, if they were awarded the SRR program would receive the first large payment. If the company fails to secure large contracts by early next year, we believe Red Cat needs to raise $15M in 2025 and possibly another $20 - 30M in order to get to profitability. We view this as one of the bigger risks for investors. However, given the company’s growing opportunities globally we believe the company will be able to raise the necessary capital to meet this aggressive growth trajectory.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Valuation

Given Red Cat is not profitable, we are using an EV/Sales multiple to value the company. Red Cat’s closest public peer is defense drone leader Aerovironment (AVAV), which is much bigger from a revenue perspective and profitable. Aerovironment is currently trading at ~6x EV/Sales based on 2025 estimates, which is also inline with our broader industrial tech comp group. Given the much stronger expected growth rate, we believe Red Cat deserves a premium multiple. However, Red Cat shares are up 235% YTD as a result of strong quarterly results, but also likely growing optimism of being awarded the massive SRR T2 program. In the event Red Cat is not awarded this contract, we expect shares to trade down materially. Furthermore, we want to reiterate that we expect Red Cat’s financial results to be lumpy on a quarterly basis, and results that fall short of expectations could put significant downward pressure on shares given the company’s sensitive cash position. That said, we believe the company’s long term growth trajectory remains very bright regardless of massive DoD contracts, which we believe will inevitably come. In the event of meaningful pullbacks, we would view it as an attractive opportunity to add to long term positions.

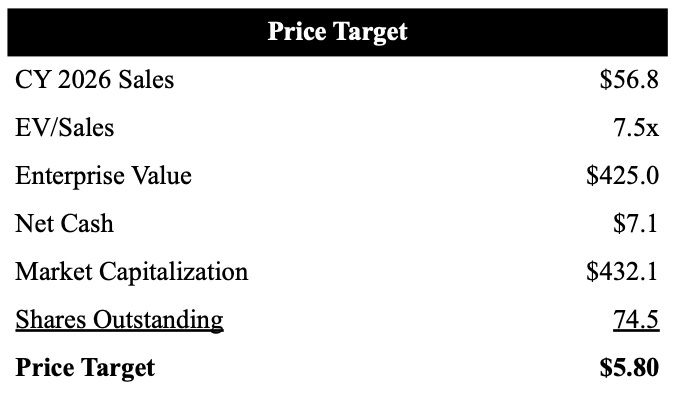

As shown below, based on our 2026 calendar year revenue estimate of $56.8M and 7.5x EV/Sales multiple, we value Red Cat shares at $5.80, which equates to ~80%+ upside at current levels.

Source: Industrial Tech Analyst

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.