Stock Report: Impinj, Robust Growth Potential As Leader In RAIN RFID, But Lofty Profitability Expectations Will Disappoint Investors (SELL)

Stock Report: Impinj, Robust Growth Potential As Leader In RAIN RFID, But Lofty Profitability Expectations Will Disappoint Investors (SELL)

We are excited to publish our bearish stock report on Impinj PI 0.00%↑ , and why despite being a leader in the fast growing RFID market we see ~35% downside in shares.

Company Overview: Impinj is a leading provider of radio-frequency identification (RFID) solutions that provide item intelligence and connectivity for retailers, supply chain and logistic (SC&L) operators and a number of emerging industries. Impinj's solution connects everyday items to the internet using a form of RFID known as RAIN, which was developed by the company’s current CEO. With this, businesses can identify, locate, authenticate and engage each item, which over time has significantly improved inventory management, asset tracking and overall operational efficiencies. Impinj sells an entire platform, which includes endpoint integrated circuits (ICs) to apply to items, getaway radio ICs and finished getaways that communicate with the tagged ICs, as well as software to extract item intelligence from the tag data. Impinj generates ~75% of revenues through the sales of endpoint IC where OEM partners attach an endpoint IC to a printed or etched antenna on a paper then cover the composite inlay with a paper face to form a tag and is attached to items in retail, SC&L, healthcare, automotive, industrial and manufacturing, and many more products. Impinj has sold more than 95 billion endpoint ICs since inception, and global enterprises such as Walmart, UBS and Target have deployed Impinj’s IoT platform. Impinj fulfills via a board and established global ecosystem of solution providers, system integrators and distributors, but ~44% of sales in 2023 were sold to tag manufacturers Avery Dennison (33%) and Arizon (11%). The company is traded on the NASDAQ exchange under ticker PI, and headquartered in Seattle, Washington.

Below is an overview video of Impinj’s RAIN RFID solution.

Investment Thesis: We believe Impinj is a clear leader in the fast emerging RAIN RFID industry, which we anticipate will be one of the fastest growing tech markets over the next 5 years. We believe expansion across Impinj core markets, retail and logistics, and new verticals will enable the company to see 20%+ growth return. However, elevated inventory levels at key retail customers caused revenues to decline in 2H23. Heading into 2024, elevated inventory levels remain a headwind, but we are also cautious on robust consumer spending trends continuing as we expect inflation to put pressure on discretionary spending. This in turn will likely impact Impinj’s largest markets, retail and logistics, and see the company’s 25%+ 2H24 consensus growth expectations as aggressive. Furthermore, we believe investor focus has now turned to profitability, which current consensus estimates are calling for EBITDA to triple from $21M in 2023 to $62 in 2025. We believe a challenging operating environment, coupled with possible pricing pressure from Impinj’s largest customers puts these current estimates at risk. A combination of near term growth headwinds and lackluster profitability is not a good combination for a company trading at ~55x EV/EBITDA based on 2025 estimates. In turn, we see ~35% downside in shares with a $80.93 price target.

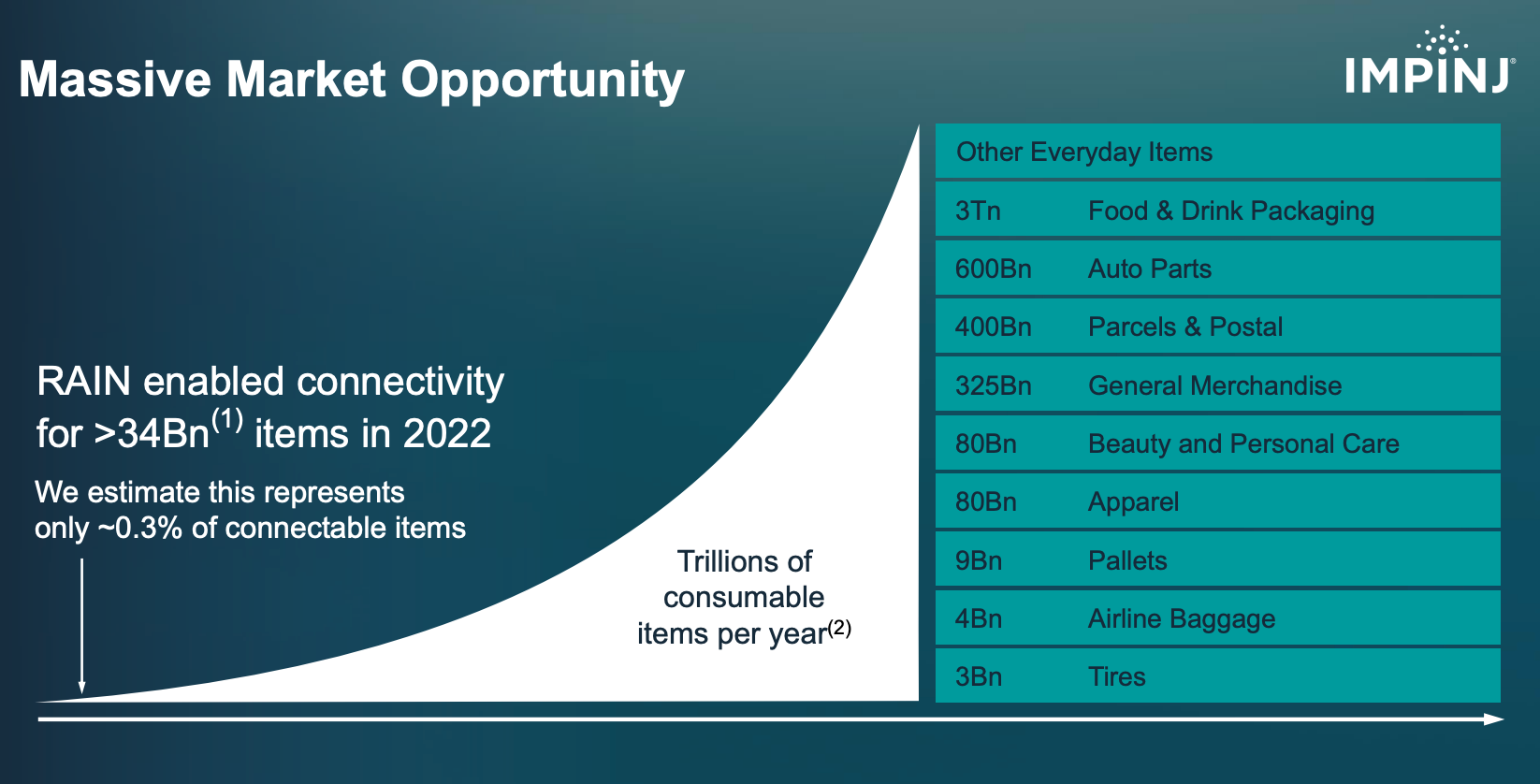

Under-penetrated RAIN Market Growing 29%+: According to Impinj’s 4Q23 investor deck, there were an estimated 34B items tagged with RAIN ICs endpoints in 2022. As shown below, the number of ICs deployed has seen a 29% CAGR from 2012 - 2022. When comparing the number of annual deployments to the total number of possible taggable items, Impinj estimates that their current penetration rate is 0.3%. When considering the possible deployments beyond retail and logistics, the company sees a total addressable market of a trillion annual deployments across food packaging, auto, beauty and personal care and more industries as shown in the exhibit below. We believe RAIN RFID is the way of the future, and given the large addressable market we believe this industry will continue to grow 20%+ over the next 5 years. We expect Impinj’s market leadership will allow the company to see similar growth as the overall industry. Other providers of IC endpoints include NXP, EM Microelectronic, Kiloway, Quanray, Shanghai Fudan Microelectronics Group, Alibaba and Alien.

Source: Impinj 4Q23 Investor Presentation

Source: Impinj 4Q23 Investor Presentation

High 2H24 Expectations In Challenging Operating Environment: Although upbeat on the long term opportunity for RAIN RFID, we believe challenging market dynamics will continue to hinder growth in the near term for Impinj. The challenging operating environment continues to be led by elevated inventory levels with retail customers, but we see additional risk with a slow down in discretionary consumer spending. We believe persistent inflation has pushed the cost of living to a very challenging level for many consumers, and foresee this to ultimately slowdown discretionary spending. We believe this would directly impact Impinj’s two biggest verticals, retail and logistics. While current consensus estimates are calling for Impinj revenues to decline ~11% Y/Y 1H24, analysts are currently forecasting ~30% Y/Y growth in 2H24. Until we see further evidence of improving market dynamics we are hesitant to believe the company will show revenue growth in 2024, and believe current revenue estimates are at risk of coming down.

Lofty Profitability Expectations: We also anticipate a big headwind Impinj could experience could come from pricing as key customers push for concessions. The number of endpoint IC providers has increased over the last several years and coupled with the increase in IC endpoint volumes gives customers the advantage in price negotiations. For example, on Avery Dennsion’s (33% of 2023 sales) 4Q23 earnings call, its management highlighted that raw material costs declined in 2023. Impinj saw non-GAAP gross margins decline 360 bps Y/Y to 51.9% in 2023. Although we believe it can generate strong adjusted EBITDA, current consensus estimates are calling for adjusted EBITDA to triple from $21.8M in 2023 to $59.4M in 2025. We believe a challenging operating environment, coupled with possible pricing pressure puts these current estimates at risk.

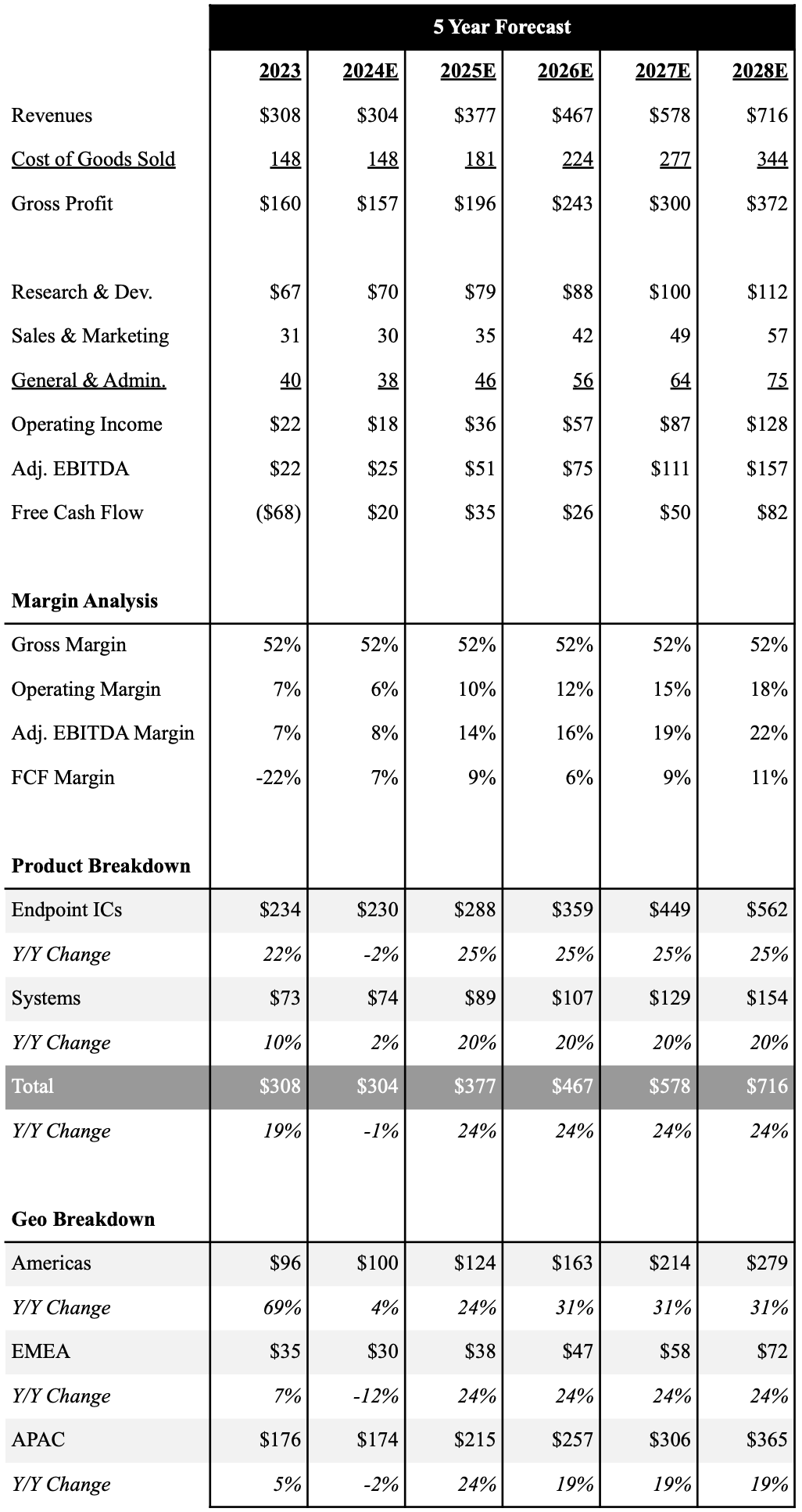

Financial Outlook: Although we expect improving inventory levels in 2H24, we expect growth to modestly improve mid-teens and expect the company to report essentially flat Y/Y growth in 2024. Our cautious near term outlook is lower than consensus estimates, which is calling for ~30% revenue growth in 2H24 and full year revenues to be up ~7% in 2024. As the operating environment improves, we do believe the company can sustain 20%+ revenue growth for the next several years as RAIN RFID becomes increasingly adopted in several industries. As stated above, we are cautious on the company’s ability to grow gross margins as key customers likely push for price concessions. In turn, our base case is the company can sustain 52% non-GAAP gross margins, but see the potential risk they may trend toward 50% overtime.

We do believe the company has a scalable operating model, but Impinj will need to continue to invest in R&D to maintain its leadership in the RAIN market. Although we do not expect meaningful revenue growth in 2024, we expect Impinj to improve operational efficiencies and see modest operating margin expansion that will result in $24.7M in adjusted EBITDA in 2024 (consensus $29.7M.) As revenues ramp up in 2025, we expect adjusted EBITDA margins to expand and generate $51M in adjusted EBITDA. However, this is also below the consensus $59.4M estimate. Assuming the company can grow in-line with the overall industry, we foresee the company hitting ~20% adjusted EBITDA margins in 2028. Management acknowledged on the 4Q23 earnings call that free cash flow generation will be a priority for the company in 2024. We expect the company to generate $21.9M in free cash flow in 2024, and believe the company could generate $80M+ per year by 2028.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

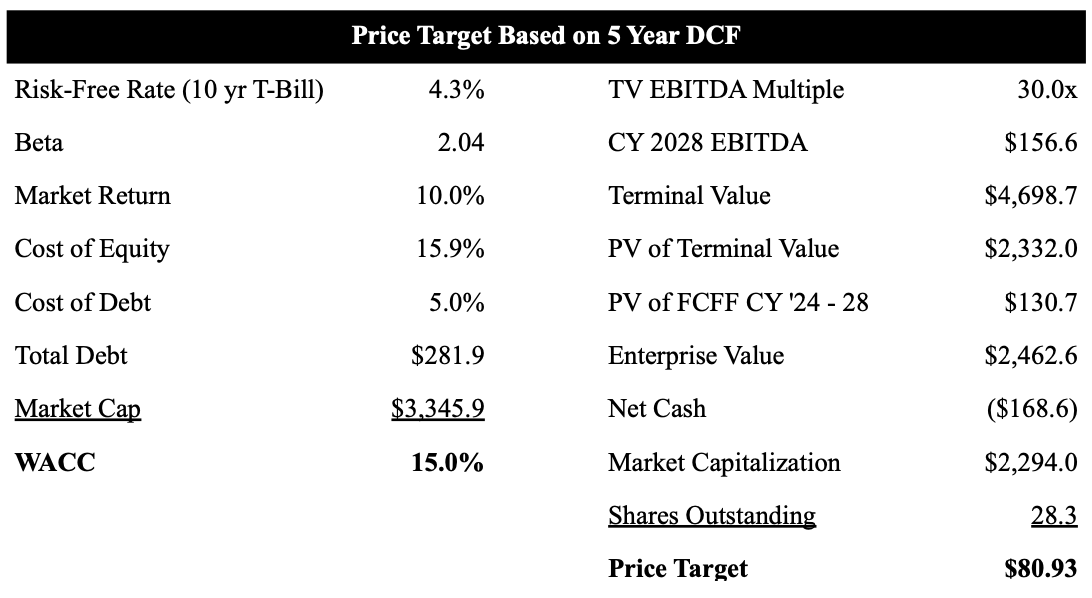

Expensive Valuation: We believe the ongoing macroeconomic concerns compounded with inventory build at OEMs creates a high level of risk for downside rather than the upside currently projected in consensus estimates and as a result we would be a seller of Impinj shares. We believe a combination of near term growth headwinds and lackluster profitability is not a good setup for a company trading at ~55x EV/EBITDA based on 2025 estimates. That said, we are upbeat on Impinj’s growth potential, and would be very interested in building a position in the event of a meaningful pullback. As shown in our table below we use a 5 year DCF model to value Imping shares. Based on our current forecast we value Impinj shares at $80.93, which equates to ~45% downside at current levels.

Source: Industrial Tech Analyst

2024 Investor Calendar

Looking to stay on top of all market moving events? Get our 2024 Investor Calendar!

Calendar includes:

US economic release dates

FOMC meeting dates

Option expiration dates

Market holidays

Historical monthly market returns

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.