Stock Report: Ondas, Driven By Leadership In Two Secular Growth Markets (IIoT and Drones) We See 350% Upside (BUY)

Stock Report: Ondas, Driven By Leadership In Two Secular Growth Markets (IIoT and Drones) We See 350% Upside (BUY)

We are excited to publish our bullish stock report on Ondas Holdings (ONDS), and why their leadership in two secular growth markets (Industrial IoT and commercial drones) could drive ~350% upside in the stock.

Company Overview: Ondas Holdings is a leading provider of mission critical private wireless connectivity and commercial drone solutions through its wholly owned subsidiaries Ondas Networks and Ondas Autonomous. Ondas Networks (~43% of 2023 sales) designs, develops and manufactures FullMAX, their patented, Software Defined Radio (SDR) platform for a wide range of mission critical IoT applications, which require secure, real-time connectivity with the ability to process large amounts of data at the edge of large industrial networks. FullMAX is addressing a growing number of mission critical applications that require more processing power in many critical infrastructure markets, such as rail, electric grids, drones, oil and gas, and public safety, homeland security and government. The Ondas Autonomous System segment (~57% of 2023 sales) designs, develops, and markets automated, AI-powered commercial drone solutions and counter-drone systems. Their FAA type certified commercial drone solution, Optimus System, provides aerial data to enterprise and government customers. Primary use cases include public safety, security and smart city deployments where automated emergency response, mapping, surveying, and inspection services are highly valued, in addition to industrial aerial data services in a growing number of commercial sectors. Their commercial drone platforms are typically provided to customers under a Data-as-a-Service (DaaS) business model, while some customers will choose to purchase an entire solution. Their counter-drone systems are utilized by government and enterprise customers to protect critical assets and people from the threat of hostile drones. Ondas Holdings is traded on the NYSE under the ticker ONDS, and is headquartered in Waltham, Massachusetts.

Investment Thesis: We believe Ondas Networks and Ondas Autonomous are strongly positioned in two robust secular tech trends that are both still in the early innings of adoption. First, Class 1 North American rail operators are in the beginning of a major network upgrade cycle. We believe Ondas Network’s FullMAX platform will be an attractive solution to drive more intelligence to the edge for rail operators, and allow the company to capture a meaningful portion of this estimated $1.3B upgrade opportunity. Second, we believe the commercial drone industry is growing into a multi-billion dollar annual market opportunity as significant advancements in automation and AI are driving adoption across a growing number of verticals. We believe Ondas Autonomous recently awarded airworthiness Type Certification for their Optimus System makes them an early leader in the quickly emerging commercial drone industry. We anticipate the combination of a robust railroad upgrade cycle and accelerated commercial drone deployments can drive 25%+ annual revenue growth over the next 5 years. Although Ondas may need to raise additional capital to fund this aggressive growth, we believe the stock accretion opportunity over the next 3 - 5 years outweighs the possibility of future dilution. Our robust outlook drives our bullish stance on Ondas shares and price target of $4.52, which equates to ~350% upside at current levels.

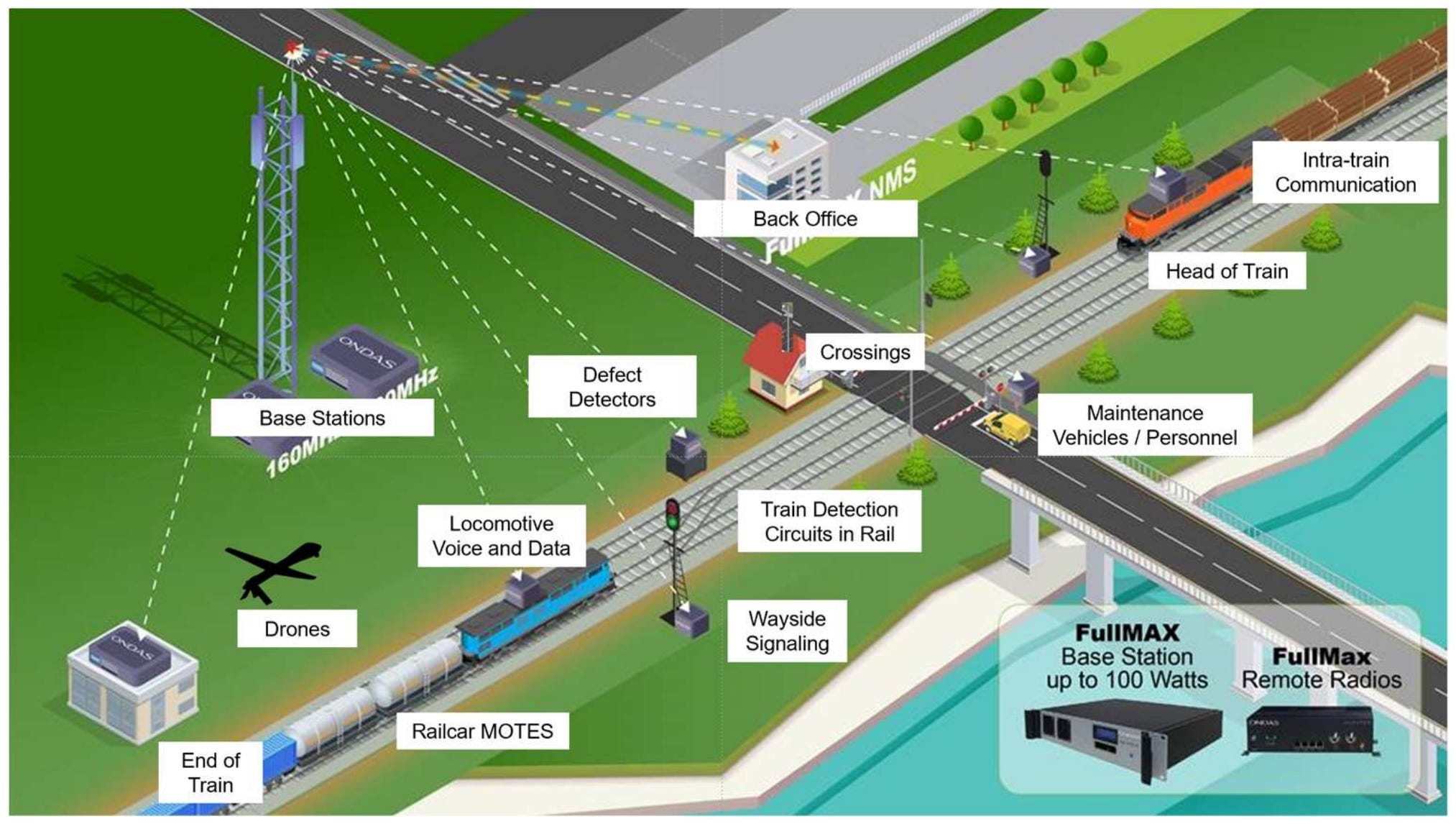

$1B+ Railroad Network Upgrade Cycle: Ondas Networks is currently targeting the North American freight rail operators for the initial adoption of their FullMAX platform driven by an estimated $1.3B upgrade opportunity. In August 2020 Class 1 rail systems in the U.S. were awarded new nationwide wideband radio spectrum by the FCC. As part of the award, the rail operators are required to vacate a series of legacy Advanced Train Control System (ATCS) networks by 3Q25 and upgrade these networks by Spring 2026. This is projected to generate a major network upgrade cycle for the rail industry. Many rail operators currently operate 20 year old legacy communication systems. These systems have limited data capacity and are unable to support increased data throughput and intelligent management systems. We believe the company’s FullMAX platform will enable the rail operators to drive more intelligence to the edge of their operating environments. Ondas estimates the North American Rail Network consists of 200,000 highway crossings, with ~65,000 of the crossings equipped with electronic systems. The Class I railroads currently operate four separate private wireless networks in support of train operations, which include 160 MHz, 220 MHz, 450 MHz and 900 MHz bands. Ondas estimates the addressable market to upgrade these four private networks is approximately $1.3B. We expect the 900 MHz network will be the first network upgraded, which is an estimated ~$450M market opportunity alone. Ondas and their strategic go-to-market partner on this opportunity, Siemens, is in late stages of integrating the enhanced ATCS with multiple railroads, paving the way for anticipated commercial volume orders and deployments in 2024. Siemens is marketing their dual mode proprietary ATCS under the brand name Airlink.

Below we highlight where Ondas’ solution can be implemented across a rail ecosystem.

Source: Ondas Holdings Investor Presentation

Commercial Drone Leader With FAA Authorization: We believe the commercial drone industry is growing into a multi-billion dollar annual market opportunity as meaningful advancements in automation and AI are driving adoption across a growing number of verticals. While many may view the drone industry as highly competitive and fragmented, we believe Ondas recently awarded airworthiness Type Certification for their Optimus System makes them an early leader in the quickly emerging commercial drone industry. This was a first of its kind certification for a non-air carrier unmanned aerial systems (UAS) or drone, which was achieved after four years of the FAA’s intensive review process. Drones with an airworthiness certificate meaningfully simplifies the waiver process to operate over people and beyond visual line of site applications. The Optimus System is already operating regularly in urban environments in the United Arab Emirates, and plans to leverage its type-certificated vehicle to conduct similar operations in urban environments across the US. We believe domestic and international drone deployments for Smart City applications to enhance public safety, industrial aerial data services in a growing number of commercial sectors and the need for counter drone technology will help drive robust revenue growth over the next 5 years.

See video for an overview of the Optimus System.

Biggest Concern Is The Need For Additional Capital: Ondas ended 2023 with $15.0M in cash and cash equivalents, and $28.5M in debt. Although they announced a $8.6M capital injection when the company pre announced in February 2024, we believe the company is likely to need to raise additional capital in the coming years. It is worth noting that on the company’s 4Q23 earnings call, Management acknowledged the possibility of spinning Ondas Autonomous off and exploring a separate IPO. Ondas is planning on hosting an Investor Day in 2Q24, which at that time we expect to hear more about the company’s long-term funding plans. That said, we believe the stock accretion opportunity over the next 3 - 5 years outweighs the possibility of future dilution, and would use any meaningful pullbacks on capital raise announcements as a buying opportunity.

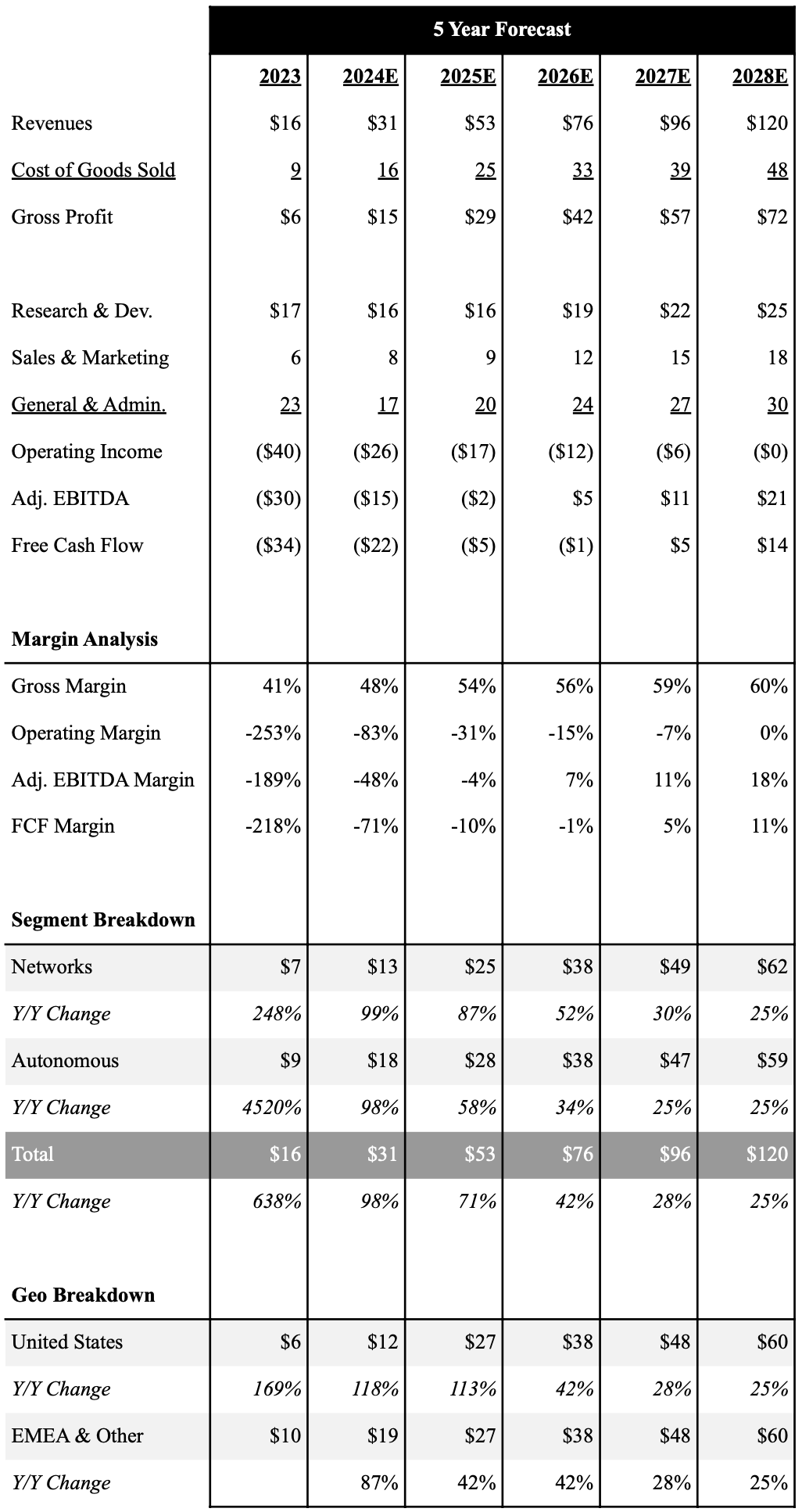

Financial Outlook: Ondas is coming off a very strong year where revenues grew 638% Y/Y in 2023 to $15.7M, which was driven by robust growth in the company’s Network and Autonomous segments. Looking into 2024, the company did not provide formal guidance on the 4Q23 earnings call, but highlighted they expect to experience significant growth in 2024. We suspect the company will provide longer term financial targets at the company’s Investor Day in 2Q24. That said, we expect strong tailwinds that drove the business in 2023 to continue into 2024, and forecast sales growing 98.3% Y/Y to $31.1M. However, we believe revenues on a quarterly basis will be lumpy given there is some uncertainty around the timing of these large railroad and commercial drone deployments. Beyond 2024, we expect accelerating new railroad and commercial drone deployments to drive at least 25%+ annual revenue growth for the next several years, exceeding ~$120M in revenues in 2028. We do want to highlight current consensus estimates imply revenues growing ~150% Y/Y to $82.7M in 2025, which we believe is a bit aggressive. Our current 2025 revenue forecast is $53.1M. Although the TAM Ondas is addressing in both markets is massive, we believe there is risk of these estimates coming down as deployments likely take time to ramp.

Although we expect gross margins to also be lumpy on a quarterly basis due to timing of deployments, we expect gross margins to improve 770 bps in 2024 to 48.4% driven by scale efficiencies. We believe the company will benefit from further scale efficiencies in the years to come as the business scales, and exceed gross margins of 60% by 2028. Ondas reported adjusted EBITDA loss of $29.7M in 2023. We expect Ondas to report an adjusted EBITDA loss of $15.0M in 2024. As revenues scale up in the following years, we believe Ondas can exceed 17% adjusted EBITDA margins or $21.2M in adjusted EBITDA by 2028. Improving profitability will also translate into improving free cash flow, but we do expect the company needs ~$30M in additional capital to fund our current growth trajectory.

Below is an overview of our 5 year outlook with a full financial model here.

(GAAP Financial Statements, Data In Millions)

Source: Industrial Tech Analyst

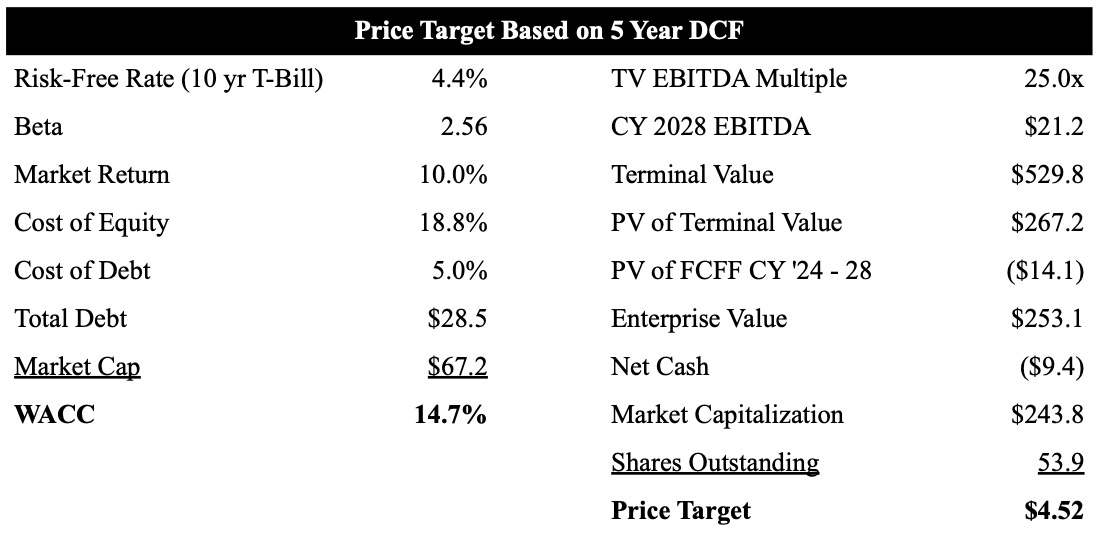

Valuation: Ondas is currently trading at 1.1x EV/Sales based on 2025 estimates, which is below our high-growth industrial tech comp group average of ~5x. Given the company’s growth prospects we believe shares are significantly undervalued, and see the opportunity for multiple expansion as revenues continue to ramp. As shown in our table below we use a 5 year DCF model to value Ondas shares. Our price target is driven by a terminal EBITDA multiple of 25x, which is in-line with our high growth industrial tech comp group (here). Based on our current forecast we value Ondas shares at $4.52, which equates to ~350% upside at current levels.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.