Stock Report: Protolabs, The Clear Winner In The Digital Manufacturing Space (BUY)

Stock Report: Protolabs, The Clear Winner In The Digital Manufacturing Space (BUY)

We are excited to publish our first stock report on Protolabs PRLB 0.00%↑ , and why we believe they are the clear winner in the digital manufacturing space.

Company Overview: Protolabs is a world leading provider of digital manufacturing services, such as injection molding, CNC, 3D printing and sheet metal fabrication. Through a combination of Protolabs Factory capacity, and Protolabs Network, which unlocks advanced capabilities and volume pricing through its highly vetted manufacturing partners, the company offers a one stop manufacturing source for prototyping to high-volume part production. Protolabs is headquartered in Minnesota, and traded on the NYSE under the ticker PRLB.

Investment Thesis: From 2012 - 2018, Protolabs was a fast growing tech company with 20%+ operating margins, but increased competition and questionable acquisitions caused growth to slow and margins to compress. However, in 2021, Protolabs acquired 3D Hubs (now branded as Protolabs Network), which is a digital manufacturing marketplace similar to Xometry. Since the acquisition, Protolabs has grown Network revenues from $33.4M in 2021 to $82.6M in 2023. We believe the combination of Protolabs Factory and Network business positions the company as a clear leader in the digital manufacturing space. We expect the combination will allow Protolabs to acquire new customers, and more importantly grow wallet share per customer given the company’s internal manufacturing capabilities. While we believe gross margins could be lumpy as the Network business ramps, we believe Protolabs will continue to grow and produce strong free cash flow. Protolabs is currently trading at 9.5x EV/EBITDA based on 2025 estimates, which is well below the company’s 5-year average of ~20x. We believe as the manufacturing environment improves, stronger growth coupled with improving margins will drive multiple expansion back towards historical levels. These all support our bullish stance, which drives our price target of $50.35.

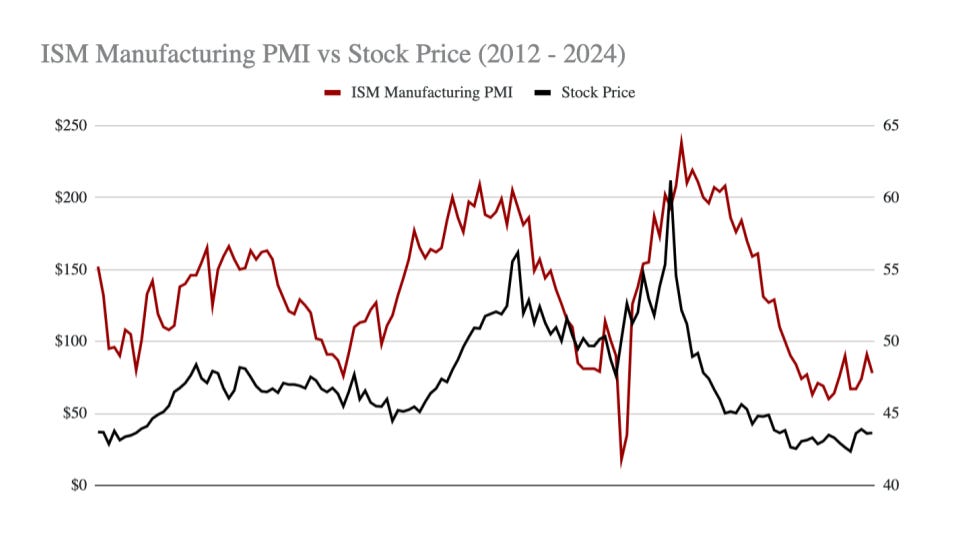

Successfully Navigating A Challenging Manufacturing Environment: Despite operating in a more challenging manufacturing environment as a result of high interest rates, Protolabs has continued to grow over the last 2 years. A large driver of this growth has been the company’s Network business, which grew 70.4% Y/Y to $82.6M in 2023. On Protolabs 4Q23 earnings call they acknowledged 2024 started off slower than expected, but the company is still expecting to grow in 2024. Although it is hard to predict when the manufacturing environment improves, we believe when that time comes, Protolabs will be in position for revenue growth to accelerate. As shown below, Protolabs stock performance has historically traded higher as the overall manufacturing sector grows as indicated by the ISM Manufacturing PMI.

Source: FactSet

Protolabs Better Positioned Than Xometry: We can not deny that Xometry has been a true disrupter to the digital manufacturing space as their Marketplace revenues have grown from ~$80M in 2019 to ~$395M in 2023. Over this time frame, we believe Xometry was able to take share from Protolabs, but with their own manufacturing network Protolabs has found its footing and we believe is now beginning to take market share back. Although based on a smaller revenue base, Protolabs Network revenues grew ~70% Y/Y in 2023 compared to Xometry’s Marketplace revenue growth of ~30% in 2023. We believe Xometry is an efficient solution to get prototypes and low-volume production parts, but as customers need higher production part orders it will not make financial sense to pay the 30-40% markup (XMTR gross margin) Xometry charges on their marketplace and rather go directly to the manufacturer. We believe the combination of Protolabs Factory and Network business positions the company much better and a clear leader in the digital manufacturing space. We expect the combination will allow Protolabs to acquire new customers, and more importantly grow wallet share per customer given their ability to produce higher production orders more economically through the company’s internal manufacturing capabilities. We believe this is already starting to show in the financials given Protolabs revenue per Customer Contracts increased by 8.7% to $9,425 in 2023. Customer Contracts is Protolabs new KPI to track growth in unique buyers. Xometry saw revenue per Active Buyer decline 10.6% Y/Y to $8,356 in 2023.

Protolabs To Consolidate Fragmented Digital Manufacturing Industry: While we are not expecting any M&A in the near term, we believe Protolabs ability to produce strong free cash flow coupled with its robust balance sheet will put the company in a good position to grow inorganically by consolidating the fragment digital manufacturing space. We believe Protolabs Network business will make it harder for smaller service bureau providers to compete, and in turn allow the company to purchase service providers at a likely discount. Although we think it is unlikely, we do see a scenario that Protolabs and Xometry merge, but would likely face antitrust scrutiny.

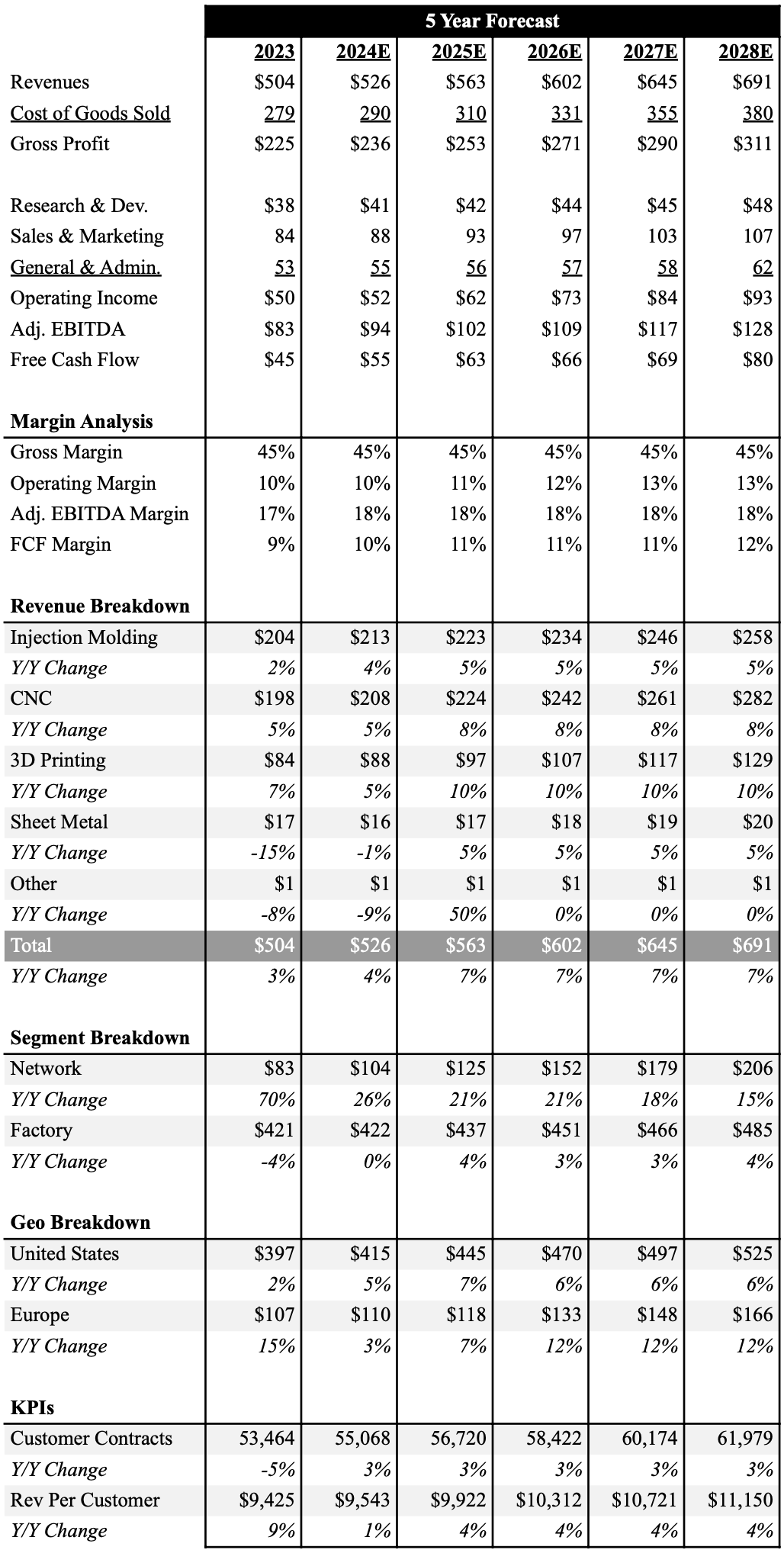

Financial Outlook: We expect Protolabs to continue to navigate a more challenging manufacturing environment and grow revenues 4.3% to $525.5M in 2024, which is slightly higher than consensus $520M estimate. We expect the company’s three biggest service offerings, injection modeling, CNC and 3D printing, to all drive growth in 2024. Looking beyond 2024, we expect the company can sustain ~7% annual revenue growth through 2028, which is in-line with the on-demand manufacturing industry. However, we believe Protolabs Factory and Network offering puts them in position to take market share. Coupled with the expectation the overall manufacturing environment should improve, we believe these estimates could end up being conservative.

We expect Protolabs Network business to continue to grow 20%+ over the next several years. Given this business has gross margins below the company average (~35%), we expect Protolabs to see limited gross margin expansion as the Network business accounts for a higher percentage of overall sales. However, we expect strong revenue growth and prudent cost management, will drive operating and adjust EBITDA margin expansion. Our current forecast expects the company to generate $94M in adjusted EBITDA in 2024, which compares to consensus estimates of $82M. By 2028, we expect the company will be generating $125M in EBITDA. We expect strong adjusted EBITDA will translate into robust free cash flow (FCF) generation, reaching $80M by 2028. However, as we stated before, our estimates imply ~7% annual growth, which could be conservative and see the potential for upward revisions to our adjusted EBITDA and FCF estimates.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

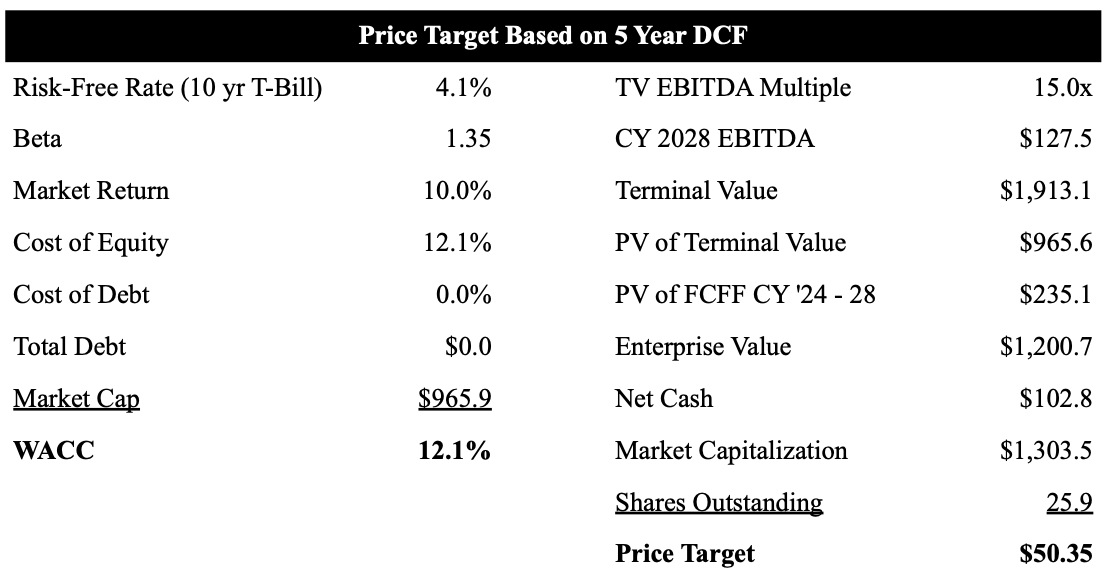

Attractive Valuation: Protolabs is currently trading at 9.5x EV/EBITDA based on 2025 estimates, which is well below the company’s 5-year average of ~20x. We believe as the manufacturing environment improves, stronger growth coupled with improving margins will drive multiple expansion back towards historical levels. As shown in our table below we use a 5 year DCF model to value Protolabs shares. Based on our current forecast we value Protolabs shares at $50.35, which equates to ~40% upside at current levels.

Source: Industrial Tech Analyst

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.