Stock Report: Robust Medical Business, Improving Profitability and Multiple Expansion Is Why We See 200% Upside in Materialise Stock!

Stock Report: Robust Medical Business, Improving Profitability and Multiple Expansion Is Why We See 200% Upside in Materialise Stock!

We are excited to publish our stock report on Materialise (MTLS 0.00%↑) , which is one of our favorite digital manufacturing stocks. Driven by a robust medical business, improving profitability and multiple expansion, we see ~200% upside in Materialise Stock.

Full analysis and 5 year financial model here.

Company Overview: Materialise is a leading provider of additive manufacturing and medical software, and 3D printing services. Their Software segment offers software that enhance the functionality of 3D printers and manage enterprise wide 3D printing workflows. The Medical segment provides medical software that allows medical-image based analysis, planning, and engineering, as well as patient-specific design and printing of surgical devices and implants. The Manufacturing segment produces 3D printed prototypes and production parts for several industrial and consumer industries. Materialise is traded on the Nasdaq exchange under the ticker MTLS, and is headquartered in Belgium.

Investment Thesis: Materialise is currently trading at an all-time low valuation despite their ability to continue to grow 10%+ over that last 2 years in a tough macro environment. While weakness in the stock performance has been largely attributed to poor sentiment across the entire additive manufacturing sector, we believe shares have been significantly oversold. Demand for 3D printing patient specific surgical tools and implants continues to rise, and driven by pent up demand for elective surgeries, we expect the Medical business to continue to see 15%+ growth for the next several years. Furthermore, the Manufacturing segment has positioned itself as a leading service provider of 3D printed production parts, which we expect to drive 10%+ growth. Lastly, we expect profitability to improve under the company's new CEO. Materialise is currently trading at a 6x EV/EBITDA multiple based on 2024 consensus estimates, which compares to the 5-year average of 40x. These all support our bullish stance and expectation for multiple expansion, which drives our price target of $17.58 and equates to ~200% upside at current levels.

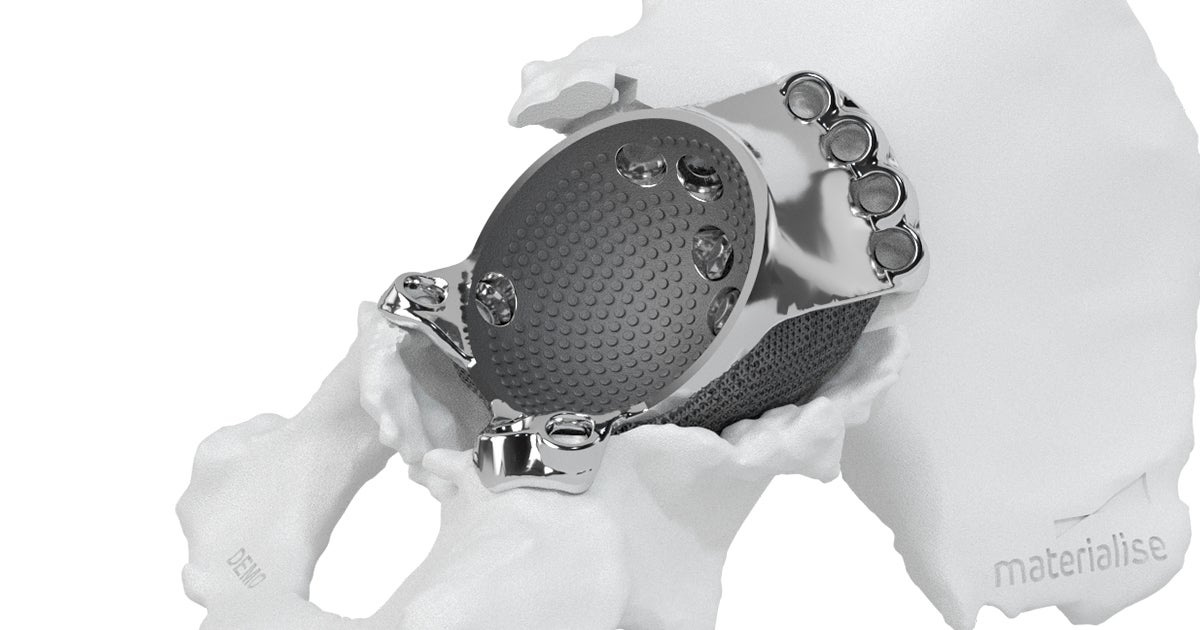

Robust Medical Business: Hospitals and surgeons across the globe have been one of the biggest adopters of 3D printing technology. Rather relying on standard off-the-shelf medical devices, 3D printed patient specific guides and implants significantly improve surgical outcomes and recovery times. (Below is a picture of a 3D printed hip implant from Materialise). We expect the company’s leadership in medical 3D printing to drive 15%+ annual growth in the Medical business for the next 3+ years. A big driver of growth will be continued expansion into the US market, as Materialise opens a new medical facility in the US. We also believe there is pent up demand for elective surgeries, which will support growth in 2024. That said, the Medical business already generates ~€100M in annual revenue. When you couple this growth, with the company’s ~30% Medical segment EBITDA margins and a conservative 15x EBITDA multiple, you get a value that is greater than the company’s current market cap alone…

Source: Materialise

Production Applications Will Drive Manufacturing Business: Materialise has built a robust 3D printing service bureau with a strong focus on production applications. We believe this segment will continue to see double digit growth in the coming years, as key automotive, aerospace and consumer goods customers lean on Materialise’s services for production grade parts.

Believe New CEO To Emphasize Profitability: The company appointed Brigitte de Vet-Veithen as the new CEO, starting Jan 1st, 2024. Mrs. de Vet-Veithen has been with MTLS since 2016, leading the Medical division. While extremely impressed by what the prior CEO and Founder, Fried Vancraen, has built, he historically would emphasize new R&D projects versus profitability. We believe Mrs. de Vet-Veithen will bring a profitability focus mindset to the company, which could drive meaningful margin expansion.

Financial Outlook: We expect the company to report 2023 revenues of €256M, up ~11% Y/Y, and improving profitability with 2023 adjusted EBITDA margins up 440 bps Y/Y to 12.6%. While we expect Management to take a conservative approach given the challenging macro when they provide 2024 guidance, we do expect to see another year of growth and EBITDA margin expansion in 2024 led by strength in their Medical and Manufacturing division, as well as improving margins in their Software division. Looking long-term, we think the company can conservatively sustain 10%+ annual revenue growth with EBITDA margins approaching 20% by 2028.

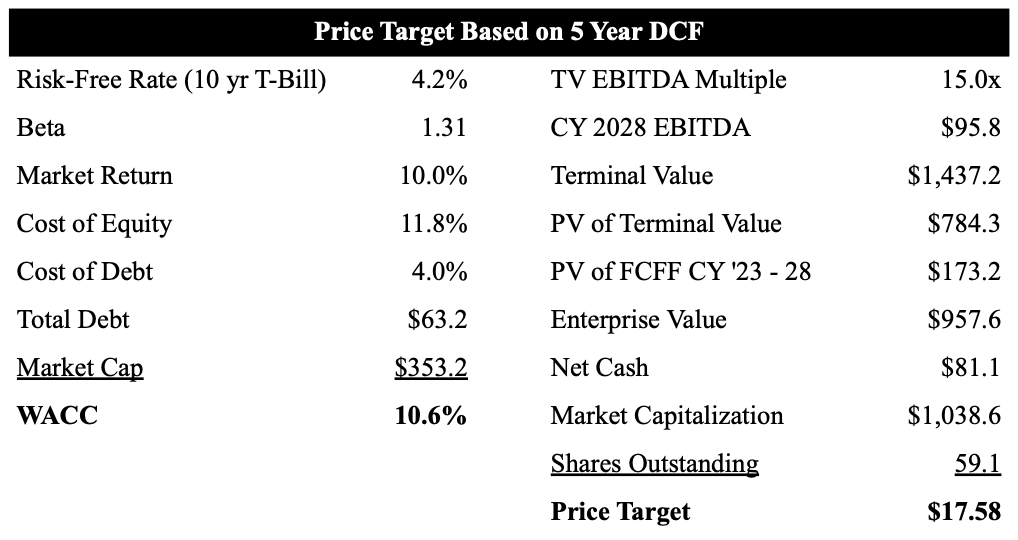

Valuation: As shown below, we use a 5 year DCF model to value MTLS shares. Based on our current forecast, which we convert into US dollars, and below average terminal EBITDA multiple of 15x, we value MTLS at $17.58 per share.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.