Stock Report: Slowing Growth & Lackluster Profits Will Disappoint Xometry Investors (SELL)

Stock Report: Slowing Growth & Lackluster Profits Will Disappoint Xometry Investors (SELL)

We are excited to publish our first bearish stock report on Xometry (XMTR 0.00%↑) , and why slowing growth and lackluster profits in 2024 is set to DISAPPOINT investors.

Company Overview: Xometry is a global online marketplace connecting buyers with suppliers of manufacturing services. Xometry uses proprietary AI-enabled technology to create a marketplace that enables buyers to efficiently source manufactured parts, and empower suppliers of manufacturing services, such as CNC, 3D printing, injection modeling and others. Xomtrey is traded on the Nasdaq exchange under ticker XMTR, and is headquartered in North Bethesda, Maryland.

Investment Thesis: We can not deny that Xometry has been a true disrupter to the digital manufacturing space as their Marketplace revenues have grown from ~$80M in 2019 to ~$300M in 2022, and proven the ability to continue to grow double-digits throughout 2023 in a tough manufacturing environment. We do believe Xometry will continue to grow, but we are cautious on the company’s ability to hit “aggressive” 2024 analyst revenue growth estimates of 25%+ with the quick emergence of new marketplace players such as Protolabs and continued challenging macro environment. Furthermore, while we believe Xometry is a great tool to secure prototypes and low-volume production parts, we believe Xometry will struggle to increase wallet share among customers. We believe this ultimately will cause the company to underwhelm investors profitability expectations. A combination of slowing growth and lackluster profitability is not a good combination for a company trading at ~125x EV/EBITDA based on 2024 estimates. In turn, we see ~45% downside in shares with a $17.61 price target.

Expecting Growth To Underperform: Xometry has seen Active Buyers, which are users who have made at least one purchase during the prior 12 months, increase 40%+ Y/Y every quarter since 1Q21. The company has been adding on average ~4,000 new buyers each quarter in 2023 and ended 3Q23 with 52,467 Active Buyers. While we believe Xometry can see Active Buyers modestly grow as they take share in a fragmented on-demand manufacturing space, we do not believe this type of growth is sustainable. Protolabs similar metric on Active Buyers, which they call Customer Contracts, was 53,464 in 2023 and remained essentially unchanged since 2021. It begs the question if Xometry will also see Active Buyers hit a plateau around this mark…Growth in Active Buyers has allowed the company to continue to grow double digits in 2023, even in a tough manufacturing environment. However, current analyst estimates are calling for 28.5% revenue growth in 2024. In order to hit this type of growth, Xometry will need to add ~4,000 new Active Buyers each quarter given Management expects average revenue per Active Buyer to remain flat in 2024. With the quick emergence of new marketplace players such as Protolabs, a continued tough manufacturing environment and the fact we think average customer spend could continue to decrease, we see downward revisions to analyst growth estimates in 2024.

Stagnant Spend Per Customer Will Underwhelm Profitability: While Active Buyers has consistently grown, average revenue per Active Buyer has continued to decline for six consecutive quarters. While a portion of this dynamic could be attributed to excess capacity throughout their manufacturing network accepting projects at lower costs, we believe it proves a fundamental flaw in the manufacturing marketplace business. When customers need prototypes and low-volume part orders, Xometry is an efficient solution. However, as customers need to go from low to high production part orders it will not make financial sense to pay the 30-40% markup (XMTR gross margin) Xometry charges on their marketplace and rather go directly to the manufacturer. We expect the lack of revenue growth per Active Buyer will pressure profitability, causing downward revisions to estimates in 2024.

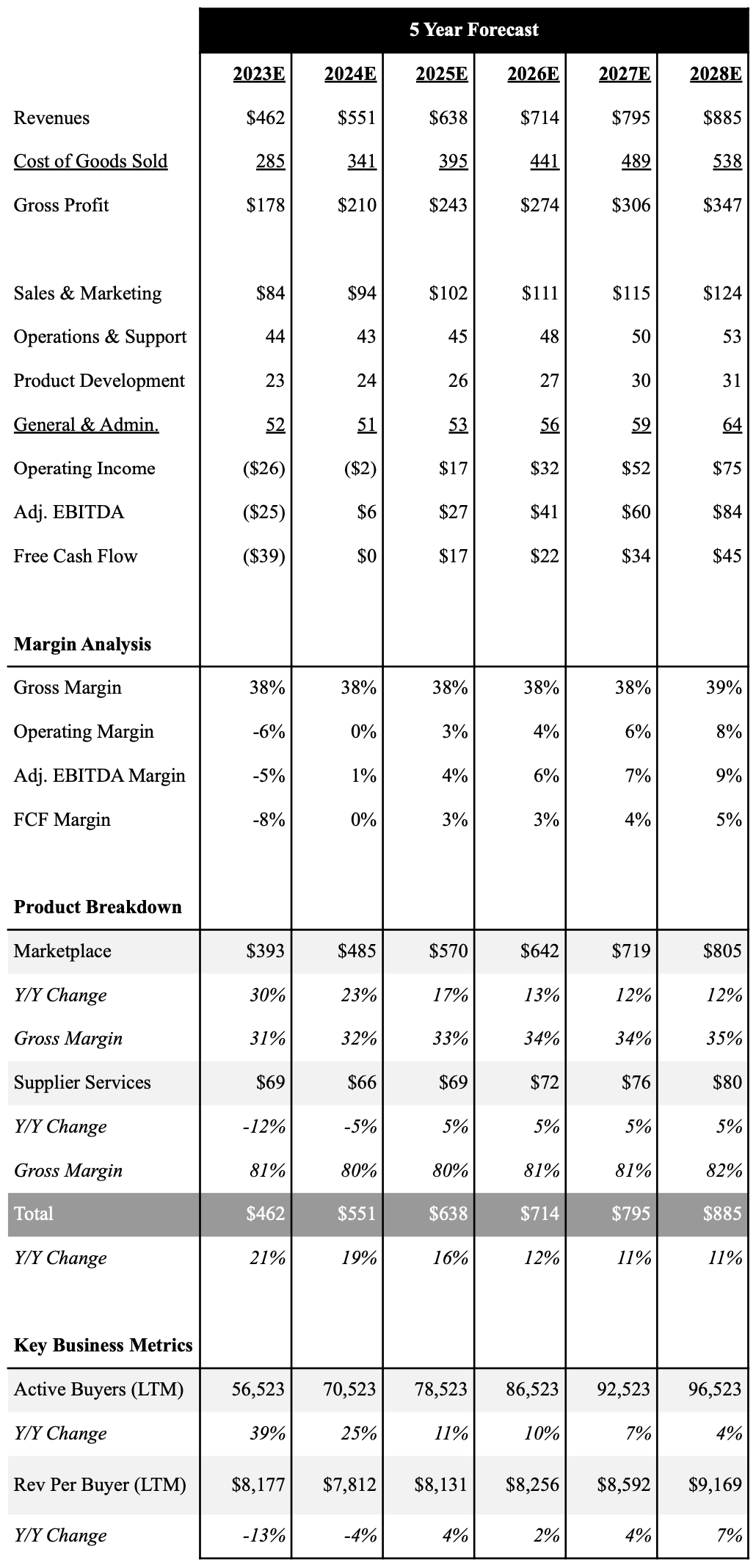

Financial Outlook: Xometry is slated to report 4Q23 earnings Thursday, February 29th, where we expect 2023 revenues to grow 21.3% Y/Y to $462.2M. While we expect Xometry to see revenues grow 19.2% Y/Y in 2024, we expect this to fall below analyst expectation of 28.5% Y/Y growth. We expect revenue growth to further decelerate to 15.9% in 2025 driven by slowing new Active Buyer growth and stagnant average revenue per Active Buyer. We expect Xometry to reach adjusted EBITDA profitability in 2024, but expect limited operating leverage will drive only $5.6M in adjusted EBITDA (consensus $11.9M). We expect Xometry to see modest EBITDA margin expansion over the next 5 years, reaching 9.5% in 2028, but will struggle to reach the company’s LT goal of 20-30%.

Below is an overview of our 5 year outlook with full financial model here.

Source: Industrial Analyst Estimates

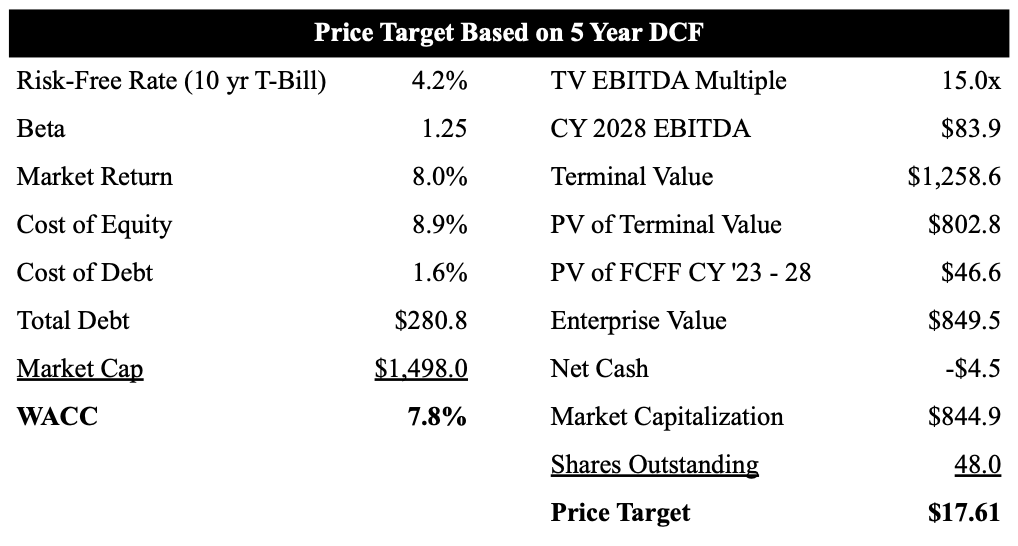

Expensive Valuation: A combination of slowing growth and lackluster profitability, is not a good combination for a company trading at ~125x EV/EBITDA based on 2024 estimates (view our Digital Manufacturing comp table here). In turn, we expect as the company underperforms current expectations, we see meaningful downside in shares. As shown below, we use a 5 year DCF model to value Xometry shares. Based on our current forecast we value XMTR shares at $17.61, which equates to ~45% downside at current levels.

Source: Industrial Analyst Estimates

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make