Warehouse Automation Leader with a Premium Price, Watching for a Pullback

View all Symbotic reports and link to our research disclaimer.

Company Overview

Symbotic SYM 0.00%↑ is an automation technology company that leverages AI-enabled robotics to create an end-to-end warehouse automation system for distribution centers. The company’s platform atomizes incoming pallets to the case level and handles those original cases throughout the system, which includes storing and autonomously re palletizing outbound orders to physical stores. The company recently began commercializing Break Pack, which is an expansion to the platform that atomizes cases to the item level to handle individual SKU orders and serve e-commerce markets. The company has seen incredible adoption with leading retailers and wholesalers in the United States, such as Walmart, Albertsons, Target, Giant Tiger, and C&S Wholesale Grocers. In addition, the company has a massive opportunity through their GreenBox venture to serve the growing demand for outsourced case handling through Warehouse-as-a-Service. Strong demand across several growing verticals has driven sales from $93M in FY20 to $1.2B in FY23, and the company has strong visibility with their order backlog reaching ~$22B as of 2023. Symbotic is traded on the Nasdaq exchange under the ticker SYM, and headquartered in Wilmington, Massachusetts.

Below is an overview video of Symbotic’s solution.

Below we present our updated core investment thesis on Symbotic, reflecting our latest analysis of the company's growth trajectory and overall profitability outlook. We include access to our downloadable 5-year financial model and our latest price target assessment.

Investment Thesis (HOLD)

We view Symbotic has a clear leader in the warehouse automation space, as their end-to-end solution has seen strong adoption across several distribution centers in the U.S. We are very upbeat on the company’s opportunity with Walmart, and their plan to automate 42 Walmart distribution centers in the US, which accounts for ~$10B of the company’s massive ~$22B backlog. Furthermore, we believe the company’s Greenbox venture to offer Warehouse-as-a-Service, expansion into the fulfillment automation market with Break Pack, as well as their recent entrance into micro-fulfillment through the Walmart acquisition positions the company for long-term success. So why are we not buyers today? Although excited about the company’s future prospects, Symbotic is trading at ~33x EV/EBITDA based on 2026 estimates. While the Company’s robust backlog can support a premium valuation, Symbotic is just becoming profitable. As the company scales up, we believe revenues and profitability may continue to be lumpy, and we are still skeptical on the company’s long-term profitability target. That said, we remain on the sidelines largely due to valuation, but would view a further pullback as a compelling buying opportunity.

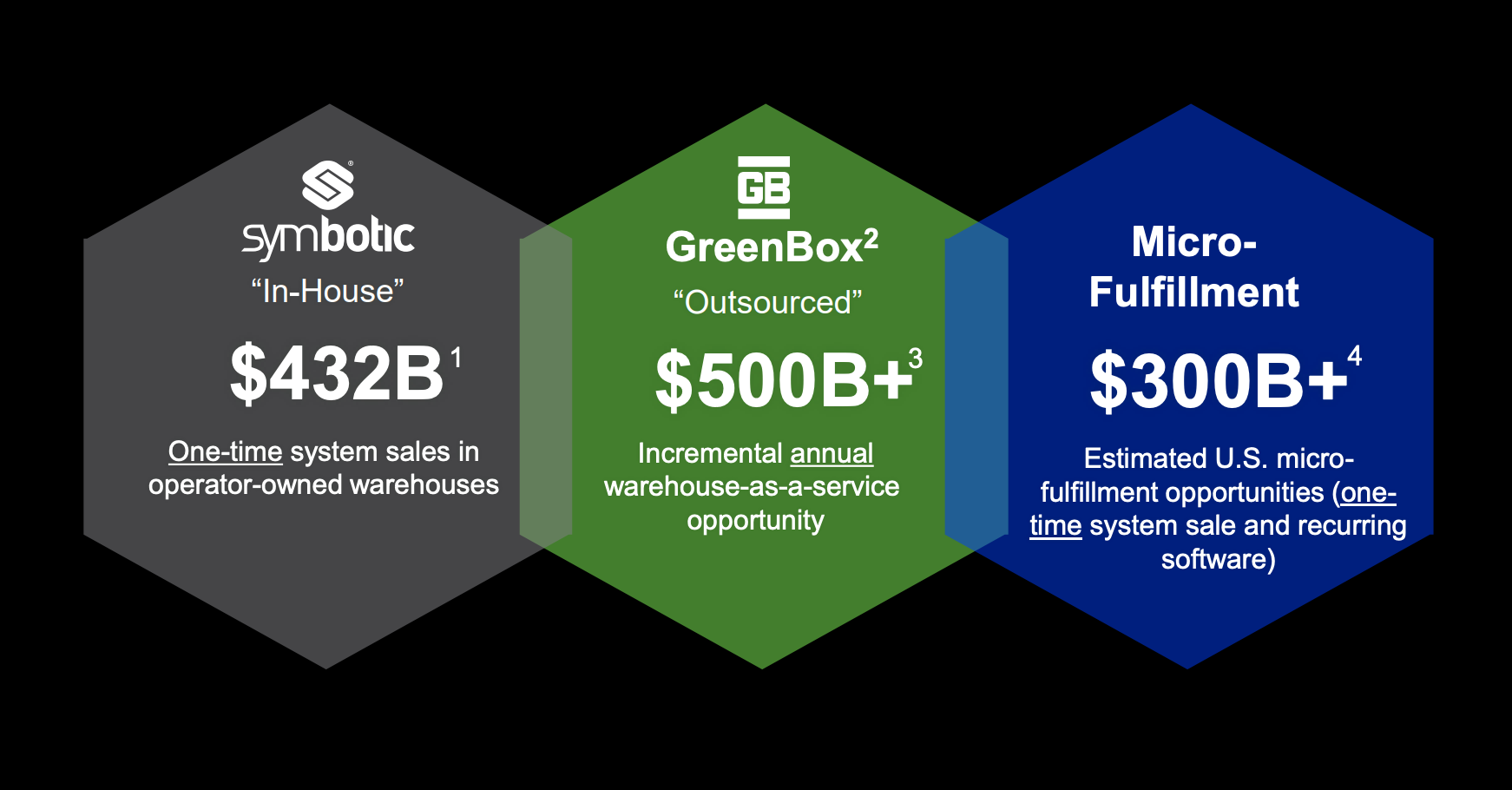

$1.2T+ Market Opportunity: Symbotic estimates its core U.S. warehouse automation market opportunity at $432B, covering general merchandise, grocery, food distribution, CPG, apparel, home improvement, auto parts, 3PL, refrigerated and frozen foods, pharmaceuticals, and electronics. Expansion into Canada and Europe could push this opportunity even higher. Beyond traditional warehouse automation, Symbotic’s GreenBox venture introduces an additional $500B+ annual market by offering Warehouse-as-a-Service, shifting the industry toward an outsourced fulfillment model. Additionally, micro-fulfillment, accelerated by Symbotic’s acquisition of Walmart’s Advanced Systems and Robotics business, presents a $300B+ U.S. opportunity, driven by one-time system sales and recurring software revenue. Combined, these segments bring Symbotic’s total addressable market to well over $1.2T, positioning the company as a dominant force in next-generation supply chain automation.

Source: Symobtic

Strong Visibility With ~$22B Backlog Led By Walmart: Symbotic has secured strong adoption from major global companies, with Walmart remaining its largest and most strategic customer. Walmart has been engaged with Symbotic since 2015, initially agreeing in 2021 to install 80 modules across 25 of its 42 regional distribution centers. In May 2022, Walmart expanded this partnership, committing to 168 modules across all 42 U.S. facilities, contributing an estimated $10B to Symbotic’s ~$22B backlog. Beyond distribution centers, Symbotic is expanding into micro-fulfillment through its recent acquisition of Walmart’s Advanced Systems and Robotics business. This move not only extends Symbotic’s reach into store-level fulfillment but could also add over $5B to the company’s backlog, driven by Walmart’s commitment to deploy automation in 400 Accelerated Pickup and Delivery (APD) centers, with the potential for further expansion. Additionally, Symbotic has a massive growth opportunity through its GreenBox venture, addressing rising demand for Warehouse-as-a-Service. Established in July 2023 as a joint venture with SoftBank Group, GreenBox aims to build and automate global supply chain networks using Symbotic’s advanced AI-driven automation technology. Symbotic and SoftBank hold 35% and 65% ownership, respectively, and the initial GreenBox agreement added $11.5B to Symbotic’s backlog. With a total backlog now exceeding $22B+ and growing, Symbotic is well-positioned to capitalize on the accelerating shift toward warehouse and fulfillment automation across distribution centers, outsourced logistics, and retail micro-fulfillment.

Recent Performance

Below we present a snapshot of Symbotic's recent financial performance, as well as other key performance indicators. Additionally, access our financial model below, which provides more historical results for a deeper analysis.

Source: Symbotic; Data In Millions

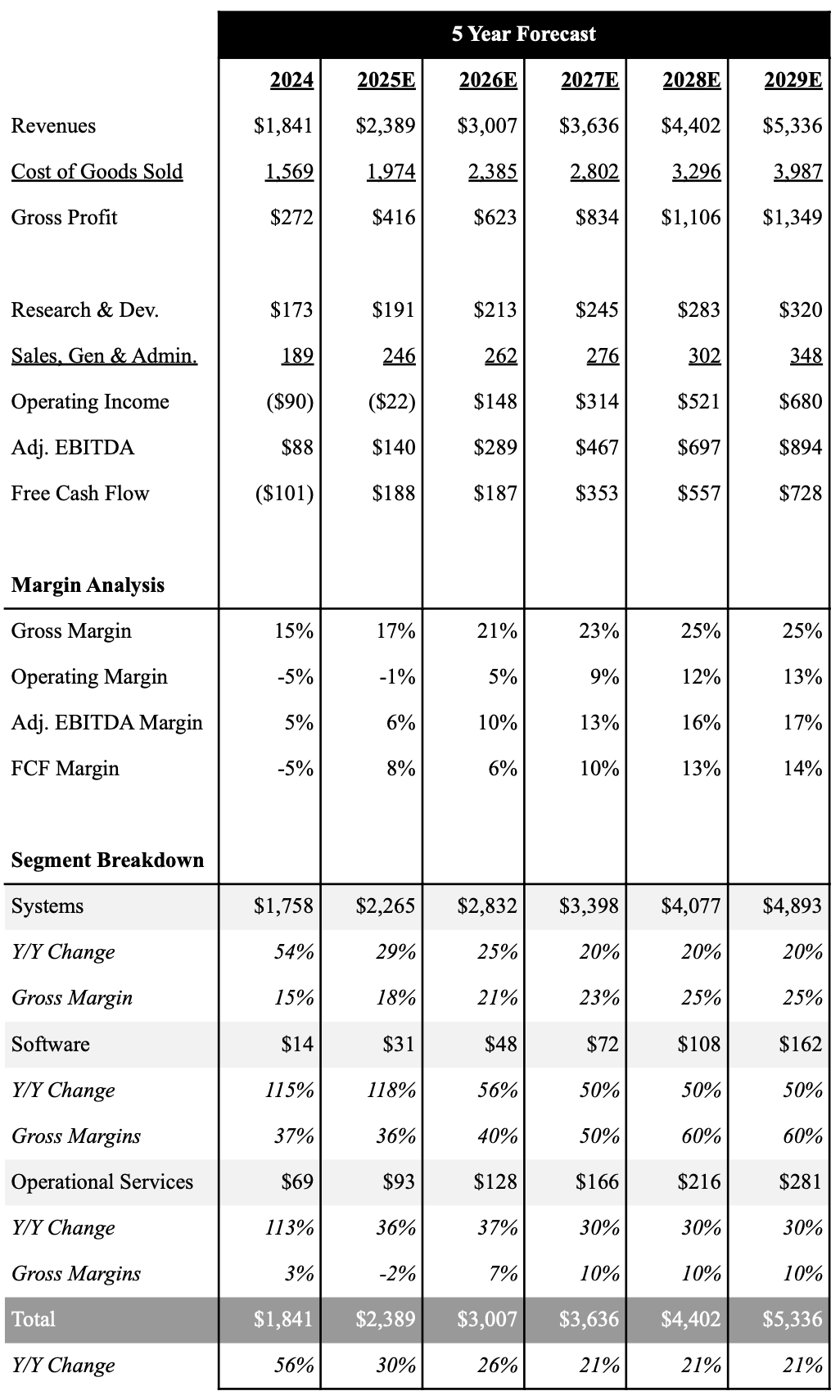

5-Year Financial Outlook

Given Symbotic’s ~$22B+ backlog, we believe the company has incredible visibility for the next several years, and it is now in the hands of Symbotic’s ability to ramp up deployments. However, as we have seen over the fast few quarters scaling up these deployments has proven to be lumpy and difficult. As a result we have taken down our FY25 estimate slightly, but do believe sustaining 30% growth is becoming more difficult. In turn, we believe a 20% growth rate through 2029 is more appropriate.

Although gross margins were down 130 bps in FY24, we expect gross margins to expand on an annual basis as the company continues to scale, and can approach ~25% by FY28. We believe the company can sustain adjusted EBITDA profitability going forward, and expect the company to report adjusted EBITDA of $140.3M in FY25 and $289.3M in FY26. However, not that these targets imply ~6% and ~10% adjusted EBITDA margins, meaning the company will need to continue to grow 25%+ to hit these numbers. Long term, we think Symbotic can exceed mid-teen adjusted EBITDA margins at scale. We also expect the company to continue to generate strong free cash flow to help fund the business and future R&D efforts.

Below is an overview of our 5-year outlook and link to our downloadable financial model.

Source: Symbotic, Industrial Tech Analyst; Data In Millions

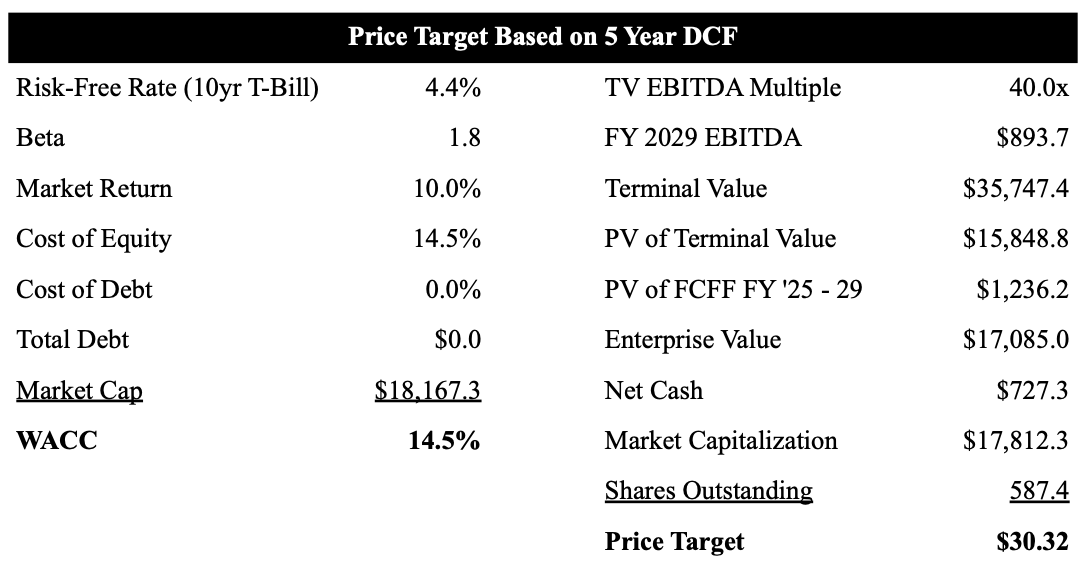

Valuation

As shown below, we use a 5-year DCF model to value Symbotic shares. Based on our current forecast and 40x EBITDA multiple on our terminal estimate we value Symbotic at $30 per share.

Source: Symbotic, Industrial Tech Analyst, Data In Millions Except Price Target

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.