Symbotic Delivers Blowout FQ4, Achieves Profitability but Valuation Concerns Persist

View all Symbotic reports.

Key Takeaways: Symbotic SYM 0.00%↑ delivered impressive FQ4 2024 results, which significantly surpassed consensus expectations and the company achieved its first quarter of positive net income. Revenue came in at $576.8M, well above Management’s prior guidance ($455-475M) and consensus estimates $470.2M. Furthermore, the revenue upside, robust gross margin expansion and strong cost controls resulted in adjusted EBITDA of $54.6M, which also far exceeded Management guidance ($28-32M) and topped Street expectations ($31.1M). These results underscore accelerated deployments for the company’s AI-enabled robotics solutions and effective cost management driving profitability. The upbeat momentum extended into guidance for Q1 2025, with revenue projected between $495 - 515M, which was ahead of consensus ($495.7M). However, adjusted EBITDA guidance of $27 - 31M was below consensus expectations ($42.2M). Driven by the company’s strong results and transition to profitability propelled shares up over 30% in pre-market trading, reflecting investor confidence in its growth trajectory and profitability.

While Symbotic’s FQ4 results and profitability milestone are commendable, we maintain our neutral rating on the stock due to concerns about valuation and elevated profitability expectations. Valuation remains a concern as it already reflects significant optimism about future performance by trading at ~50x EV/EBITDA based on 2025 estimates heading into earnings. Symbotic’s current forward multiples appear stretched relative to peers, particularly given its FQ1 adjusted EBITDA lagged behind consensus expectations and analyst were calling for adjusted EBITDA to grow form $106M in FY24 to $260M in FY25. While the company’s strong execution and market leadership are undeniable, we believe these factors are fully priced into the stock at current levels. In addition, we believe the company is planning to accelerate sales and marketing spend in 2025 to expand into new verticals and geographies. We would not be surprised if these expenses are likely higher than investors are anticipating and could impact profitability expectations. That said, we continue to view Symbotic as a clear leader in the warehouse automation space that has a massive $20B+ backlog driven by Walmart and growing customer list. Given results can be lumpy quarter-to-quarter due to the size of these deployments, we believe patients investors will have better opportunities for more attractive entry points.

View detailed historical results in our full financial model here.

Source: Company Filings, FactSet; Data In Millions

Investor Gifts

Looking to become a better investor or need to find that perfect gift for your finance friend? Check out these products from our partner Investor Gifts like their Premium Option Trading Computer Mat.

SAVE 20% with our exclusive promo SAVE20 at checkout!

Key 4FQ24 Earnings Takeaways

Symbotic reported robust Y/Y sales growth of ~47%, with revenue increasing to $576.8M from $391.9M in FQ4 2023. The growth was driven by a record number of new deployments for for its AI-powered robotic systems, which accounted for the majority of sales, along with expanding software maintenance and operational services offerings. The Company started a record 9 new deployments and finished 4 deployments in the quarter, bringing the total number of deployments to 44 and fully operational systems to 25. The company announced that their total customer base is now at 10, after they announced a new strategic partnership with Walmex, Walmart’s Mexico locations. The plan is to implement Symbotic's warehouse automation system in two of the retailers locations in Mexico, which added ~$400M to the backlog. Furthermore, the company announced the commencement of a second Greenbox site in Georgia. The company did not provide an updated backlog number, but we estimate it remains ~$20B+.

Gross margin for FQ4 2024 improved to 18.8%, recovering from 15.0% in the prior year, supported by better cost management and operational efficiencies. Operating expenses decreased by ~24% Y/Y to $85.5M, reflecting targeted reductions in R&D and SG&A expenses. Adjusted EBITDA saw a dramatic increase to $54.6M, compared to $13.3M in FQ4 2023, showcasing improved profitability and operating leverage. The company did burn $99.4M in cash from operations and $120.1M in FCF in quarter that was largely driven by timing of receivables. Working capital is expected to normalize in FY25.

Looking ahead, Symbotic provided guidance for FQ1 2025, expecting revenue between $495 - 515M, which implied ~37% Y/Y growth at the midpoint and exceeded consensus expectations ($495.7M). Adjusted EBITDA of $27 - 31M was below Street estimates of $42.2M. The company projected sustained revenue growth through 2025 driven by a strong sales pipeline and continued high demand for its innovative supply chain solutions. Management also highlighted plans to maintain stable gross margins while investing strategically in R&D and Sales & Marketing to expand its market leadership.

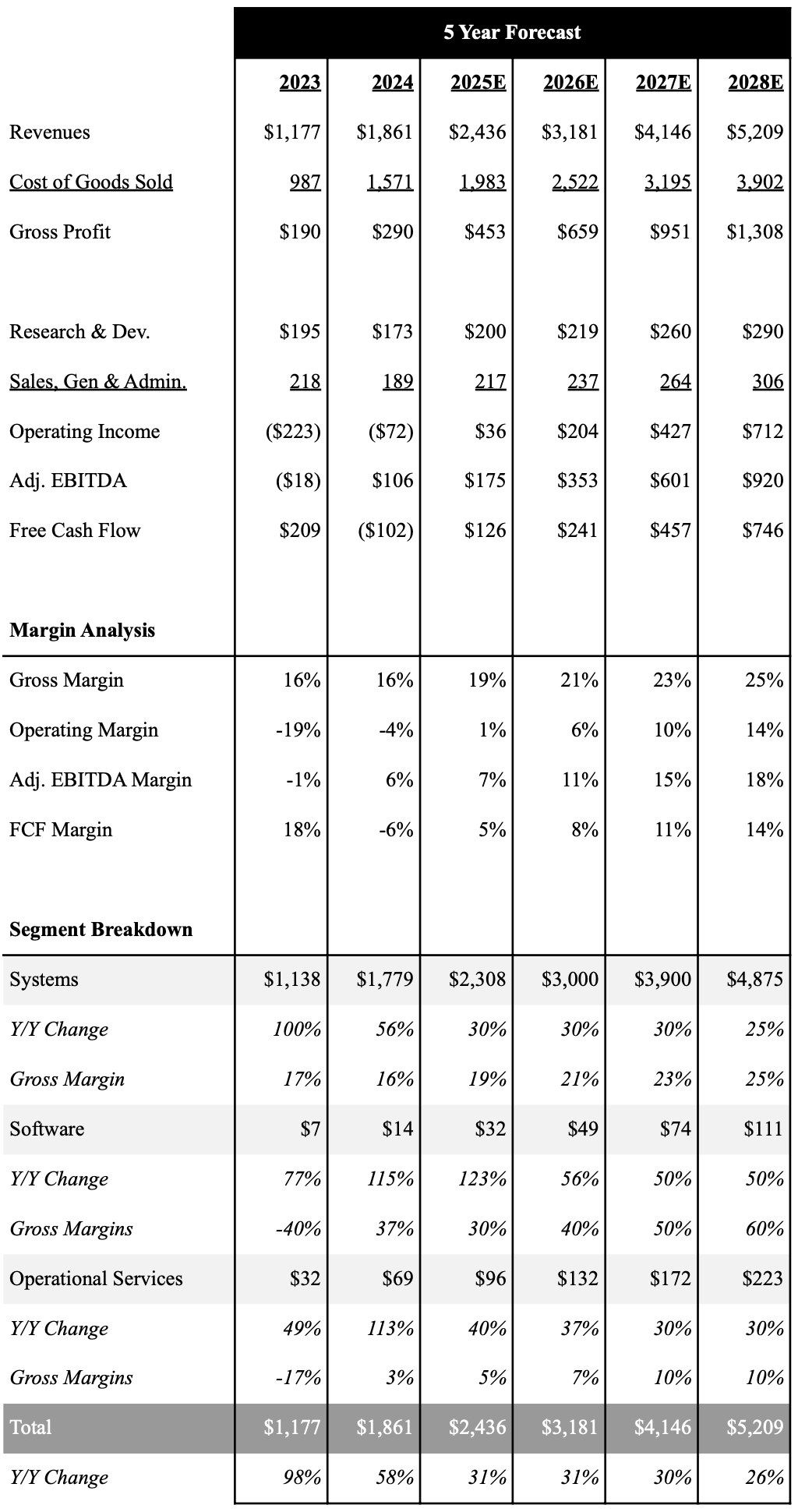

5-Year Financial Outlook

Given Symbotic’s ~$20B+ backlog, we believe the company has incredible visibility for the next several years, and it is now in the hands of Symbotic’s ability to ramp up deployments. Given the meaningful revenue beat in FQ4, we have increased our fiscal 2025 estimates. We continue to anticipate the company can sustain 25%+ growth through 2028.

Symbotic returned to solid gross margin expansion in FQ4, and we expect this trend to continue as revenues ramp. We expect gross margins to continue to expand on an annual basis, and can approach ~25% by FY28. We believe the company can sustain adjusted EBITDA profitability going forward, and expect the company to report adjusted EBITDA of $175.1M in FY25 and $353.5M in FY26. Long term, we think Symbotic can exceed ~17%+ adjusted EBITDA margins at scale, which is slightly higher due modestly lower opex assumptions driven by strong cost controls. We also expect the company to continue to generate strong free cash flow to help fund the business and future R&D efforts.

Below is an overview of our 5 year outlook with a full downloadable financial model here.

Source: Industrial Tech Analyst, Data In Millions

Investment Thesis

We view Symbotic has a clear leader in the warehouse automation space, as their end-to-end solution has seen strong adoption across several distribution centers in the US. We are very upbeat on the company’s opportunity with Walmart, and their plan to automate 42 Walmart distribution centers in the US, which accounts for ~$10B of the company’s massive ~$23B backlog. Furthermore, we believe the company’s Greenbox venture to offer Warehouse-as-a-Service, as well as expansion into the fulfillment automation market with Break Pack positions the company for long-term success. So why are we not buyers today? Although excited about the Company’s future prospects, Symbotic heading into earning was trading at ~50x EV/EBITDA based on 2025 estimates, which is a significant premium to their industrial tech peers of ~30x. While the Company’s robust backlog can support a premium valuation, Symbotic is just becoming profitable. As the company scales up, we believe revenues and profitability may be lumpy, and are still skeptical on the company’s long-term profitability target. That said, we remain on the sidelines largely due to valuation, but would view a further pullback as a compelling buying opportunity.

As shown below, we use a 5 year DCF model to value Symbotic shares. Based on our current forecast we value Symbotic at $30.47, which is higher than our prior estimate of $25.22 as a result of higher revenue and profitability expectations.

Source: Industrial Tech Analyst, Data In Millions Except Price Target

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.