Symbotic Sales Continue To Inflect, But Patient Investors Will Likely Have A More Attractive Entry Point - HOLD

Symbotic SYM 0.00%↑ reported strong Q1 results with revenues and adjusted EBITDA coming in above the Company’s previous guidance and consensus expectations. Symbotic highlighted they made significant advances in both software and hardware during the quarter that accelerated deployment times, which drove faster revenue growth, higher margins and stronger cash generation than planned in the quarter. Furthermore, the company provided stronger than expected Q2 revenue guidance. Robust Q1 execution and strong outlook drove shares up ~10% immediately following the release. Note the company is hosting an investor day on May 9th and we anticipate to hear additional insights into deployments at this event.

We continue to view Symbotic as a clear leader in the warehouse automation space, and are impressed with the Q1 execution. However, heading into earnings, analysts were calling for adjusted EBITDA to grow from $159M in CY24 to $409M in CY25. The company is still scaling up deployments and we believe revenues and profitability may be lumpy. For a company trading at ~60x EV/EBITDA, we believe the current bar is set very high and any slight miss would cause shares to decline significantly. In turn, we remain on the sidelines, but would closely monitor Symbotic and watch for a pullback to start building a position.

Key Results vs Consensus Expectations

1Q24 Results

Revenue $424.3M BEAT consensus $411.2M

Adjusted EBITDA $22.5M BEAT consensus $14.7M

2Q24 Guidance

Revenue $450 - 470M vs consensus $447.5M

Adjusted EBITDA $27 - 29M vs consensus $27.1M

Key 1Q24 Earnings Takeaways

Symobtic reported 2Q24 (Mar-24 quarter end) revenues growing 59.0% Y/Y to $424.3M, which came in above Management's previous guidance ($400 - 420M) and above consensus expectations ($411.2M). Symbotic highlighted they made significant advances in both software and hardware during the quarter that accelerated deployment times and drove revenue upside in the quarter. Specifically, they called out breakthroughs in vision related to a new Nivida AI chip, as well as modularizing the software architecture to improve performance. The company finished 3 deployments in the quarter, bringing the total number of fully operational systems to 18. System sales were $401.7M and the company generated $2.6M in software revenue in the quarter. A positive surprise was the company generating $20.1M in operational services, which was up 100%+ Q/Q as a result of the increased number of operational systems. The company did not provide an updated backlog number, but we estimate it remains ~$23B. Symbotic is expecting deployments to accelerate in the back half of the year.

Gross margins in the quarter were 10.4%, but adjusting for stock based comp, depreciation and a one-time restructuring charge, non-GAAP gross margins were 19.7%. An improvement from 16.1% during the same period a year ago. Driven by higher revenue and improving gross margins, the company generated adjusted EBITDA of $22.5M, which was higher than consensus expectations of $14.7M. Symbotic generated $21.1M in cash from operations and $18.2M in free cash flow in the quarter.

Looking ahead, the Company expects 3Q24 revenues in the range of $450 - 470M, which implies 47.5% Y/Y growth at the midpoint and was comfortably ahead of analyst estimates ($447.5M). Meanwhile, adjusted EBITDA guidance of $27 - 29M was in-line with consensus expectations ($27.1M). That said, assuming Symbotic hits the low-end of their adjusted EBITDA guidance range, the Company will have generated $63.6M in adjusted EBITDA with one quarter remaining in their fiscal year. Heading into earnings, analysts were calling for adjusted EBITDA of $400M in CY25. While we believe the Company will see adjusted EBITDA grow considerably in the years to come, we believe the growth implied in current consensus models will likely end up being too aggressive. We suspect analysts will need to revise their estimates downward in the coming quarters

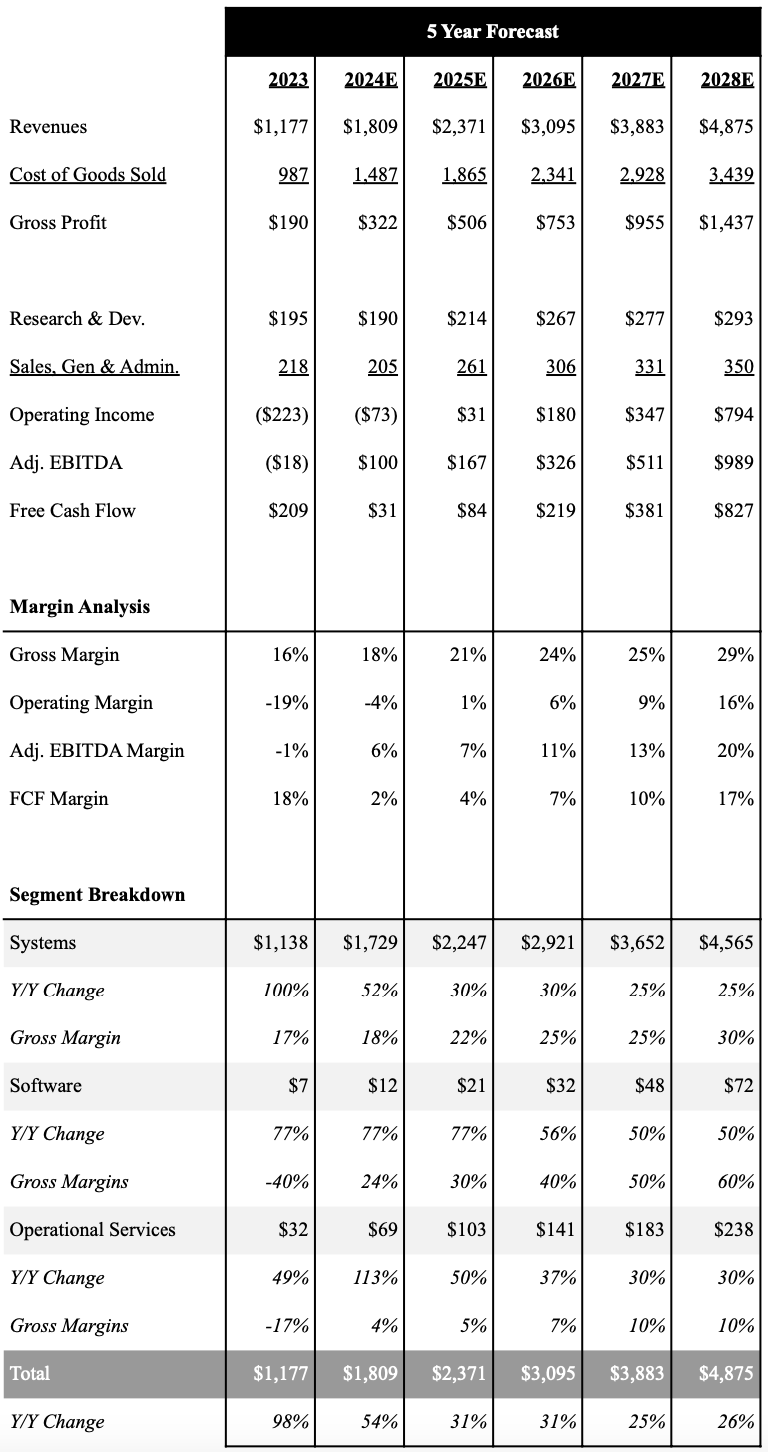

5-Year Financial Outlook

Given Symbotic’s ~$23B backlog, we believe the company has incredible visibility for the next several years, and it is now in the hands of Symbotic’s ability to ramp up deployments. Given the strong Q2 performance we did raise our revenue estimates modestly. We now expect revenues to grow 53.7% Y/Y in FY24 to $1.8B, and anticipate the company can sustain 25%+ growth through 2028. However, analysts are extremely bullish on Symbiotic future growth continuing with consensus estimates calling for revenes to grow 40%+ annually over the next 3 years. Our lower growth rate is due to our anticipation deployments this size may take a little bit longer to ramp, but their long term opportunity remains lucrative. Symbotic has seen solid gross margin expansion as revenues ramped. Although on a quarter-to-quarter basis gross margins ma ybe lumpy, we expect gross margins to continue to expand on an annual basis and approach 30% by FY28. We believe the company can sustain adjusted EBITDA profitability going forward, but are expecting meaningful operating leverage to take time as deployments scale up. We expect the company to report adjusted EBITDA of $81.5M in FY24 and $166.9M in FY25, which is well below consensus estimates coming into earnings. Long term, we think Symbotic can exceed 20% adjusted EBITDA margins at scale. We also expect the company to continue to generate strong free cash flow to help fund the business and future R&D efforts.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Investment Thesis

We view Symbotic has a clear leader in the warehouse automation space, as their end-to-end solution has seen strong adoption across several distribution centers in the US. We are very upbeat on the company’s opportunity with Walmart, and their plan to automate 42 Walmart distribution centers in the US, which accounts for ~$10B of the company’s massive ~$23B backlog. Furthermore, we believe the company’s Greenbox venture to offer Warehouse-as-a-Service, as well as expansion into the fulfillment automation market with Break Pack positions the company for long-term success. So why are we not buyers today? Although excited about the Company’s future prospects, Symbotic is trading at ~60x EV/EBITDA based on 2025 estimates, which is a significant premium to their industrial tech peers of ~25x. While the Company’s robust backlog can support a premium valuation, Symbotic is just becoming profitable. As the company scales up, we believe revenues and profitability may be lumpy and given the valuation we believe any slight miss would likely cause shares to decline significantly. In turn, we would closely monitor Symbotic and watch for a pullback to start building a position.

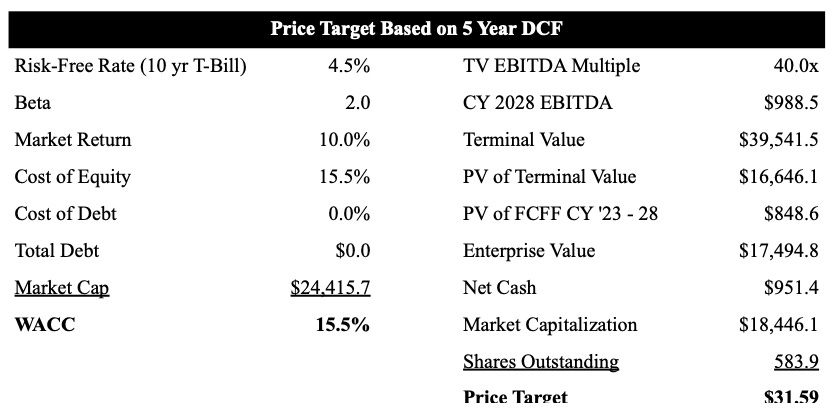

As shown below, we use a 5 year DCF model to value Symbotic shares. Based on our current forecast we value Symbotic at $31.59.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.