Tekna’s Near Term Hiccup Will Not Disrupt Their Massive Opportunity Ahead - BUY

Tekna reported 1Q24 results that were in-line with the company’s preannouncement last month. While sales in Q1 were down ~8% Y/Y largely due to timing of new system deployments and lower material sales to 3D OEMs, the company saw strong order growth continue in the quarter led by material bookings up ~25% Y/Y. Given the company’s strong pipeline, Tekna reiterated their 2024 guidance, which calls for revenue growth and margin improvements on a Y/Y basis. The company also provided bullish longer-term financial targets through 2027, which includes 25-30% annual revenue growth and ~20% adjusted EBITDA margins by 2027. That said, shares traded down ~7% on the announcement, and have traded down ~18% since the pre-announcement.

While discouraged with the Q1 revenue performance, our view on Tekna’s long-term opportunity has not changed. Given their growing pipeline and Management's very upbeat tone on the earnings call, we believe Tekna remains on track for 20%+ growth in 2024. Furthermore, despite the revenue shortfall, gross margins remained stable and we believe the company could reach adjusted EBITDA breakeven or better in 2H24. We believe Tekna is in the early innings of a multi-year super cycle as demand for their advanced metal materials and plasma systems grow across applications in 3D printing, consumer electronics, aerospace and medical. In turn, we view the near term misstep as an attractive buying opportunity for long-term investors. Assuming Tekna can execute on their aggressive growth trajectory, we believe there is 400%+ upside potential in the stock and remain strong buyers.

Key 1Q24 Earnings Takeaways

Tekna reported 1Q24 revenues of $8.7M, which was down 8.0% Y/Y. Material sales were $5.8M, which were down 9.5% Y/Y due to lower sales to 3D printer OEMs as high-interest rates have impacted new system sales. This is not a surprise as almost all public 3D OEMs have consistently reported lower system sales over the last 18 months due to higher interest rates lengthening sales cycles. That said, material bookings were $7.0M in 1Q24, up 25.0% Y/Y. This drove their materials backlog to $15.9 at the end of 1Q24, which was up 16.9% Y/Y. We believe the Company continues to see strong material demand from current aerospace customers who are ramping up additive manufacturing production, as well as the new consumer electronics opportunity with Apple and Samsung. In fact, Tekna highlighted, they provided approval samples to a new consumer electronic customer (we believe Samsung) for large scale manufacturing of smart watch cases produced by Metal Injection Molding. Although still in the early stages, Tekna expects consumer electronics to grow from 5% of revenues in 2023 to ~10% of revenues in 2024. System revenues in 1Q24 were $2.9M, which were also down 4.6% Y/Y. The revenue decline was driven by timing of deployments. Furthermore, while Q1 system bookings were down ~90% Y/Y to $0.4M, we believe Tekna has strong visibility into future orders. We specifically believe the pipeline is driven by the Company’s PlasmicSonic systems, which is used for testing materials in atmospheric re-entry conditions for space tourism and space exploration. In fact, as shown in Tekna's 1Q24 investor presentation, the Company expects order potential alone to be $5-10M in 2024, with an opportunity to grow to $287M over the next 10 years.

Despite the revenue decline we were very impressed with the Company’s strong cost controls and production efficiencies. Gross margins were 45.4%, up from 42.9% in 4Q23. Material gross margins were 34.4%, while systems gross margins were 67.4%. We believe as material revenues continue to ramp gross margins could exceed 40% and assume system gross margins will maintain ~65%. However, due to the revenue shortfall, Tekna reported an adjusted EBITDA loss of $2.6M, which included $0.7 loss related to a joint venture. Furthermore the company burned $5.0M in cash from operations in the quarter. Although upbeat about the long-term opportunity, our biggest concern is liquidity as the company ended the quarter with $10M in cash. However, this included the 3rd tranche loan ~$6M from their biggest investor, bringing their total debt position to ~$31M. That said, assuming revenues accelerate through the year, we believe the company has enough liquidity to reach profitability.

Tekna reiterated their 2024 guidance, which calls for revenue growth and margin improvements on a Y/Y basis. However, Tekna also provided updated longer-term targets from 2024 -2027. This includes revenues to grow 25 - 30% per year and adjusted EBITDA margins to reach ~20% by 2027. Tekna also provided some granular longer term targets on the material business. Tekna expects the material business to generate ~$70M in annual sales by 2027, which was in-line with our previous estimate. This will be driven by increased production capacity, as well as improving operational efficiencies. The Company had ~5 material atomizers producing additive materials in 2023, which generated $4.7M sales per machine. The Company will be adding 3 more material atomizers by 2027 and plan to increase revenue per system to at least $7.5M. However, Management indicated they have necessary capacity to keep up with near term demand.

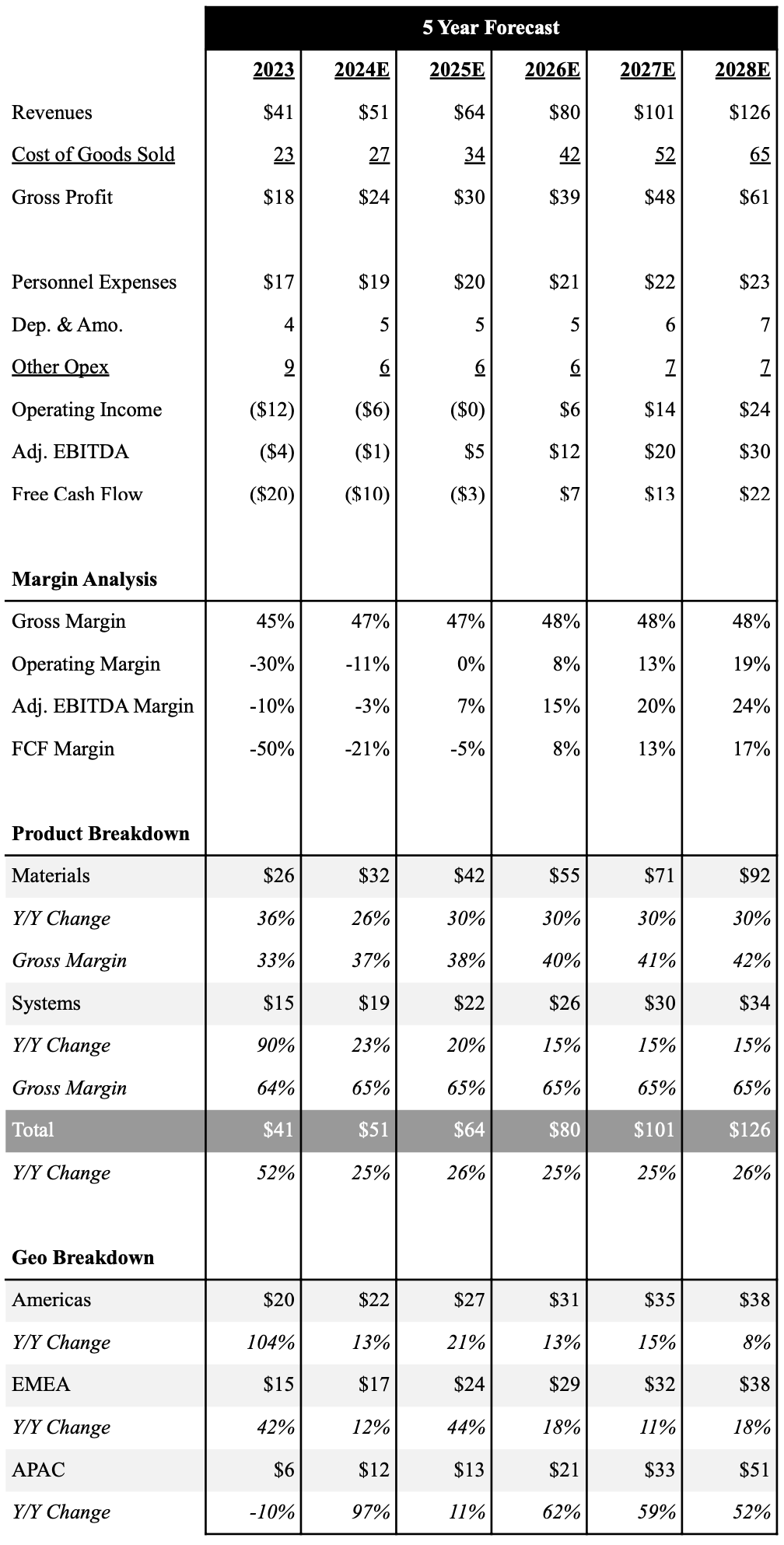

5-Year Financial Outlook

Following 1Q24 results our long-term financial outlook is mostly unchanged as it was already aligned with Tekna’s new long-term financial targets. We believe the material business will continue to grow 25%+ in 2024, driven by strength from key consumer electronic and aerospace customers. Coupled with 23% growth in system sales, we expect the company to report revenues of $51.0M in 2024, up 24.6% Y/Y. We expect the company to sustain 25%+ revenue growth through 2028. That said, we are only in the early innings of this consumer electronic opportunity with Apple and Samsung. Coupled with the ramping PlasmicSonic opportunity for Space Exploration applications, we believe these estimates could end up being conservative based on how fast these opportunities ramp.

We expect production efficiencies and cost controls will now drive gross margins up 260 bps to 47.2%. However, given the Q1 shortfall, we expect Tekna to report a small adjusted EBITDA loss of $1.5M in 2024. However, we believe the company will turn adjusted EBITDA positive beginning in 2025 and reach ~$30M in adjusted EBITDA by 2028. We expect this will translate into strong cash flow generation with our current estimates forecasting free cash flow of $21.9M in 2028.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Investment Thesis

We believe Tekna is in the early innings of a multi-year super cycle as demand for their advanced metal materials grow across applications in 3D printing, consumer electronics, aerospace, and medical. However, what makes us extremely bullish on Tekna are the key wins they received with Apple and Samsung to supply the leading smartphone providers with titanium for the casing of next gen smartphones and smartwatches. We expect Apple and Samsung to adopt titanium into an increasing number of smartphones, wearables, and other devices in the coming years, which could drive demand for 2,500 tons of titanium or $200M in sales alone. Coupled with growing demand for PlasmicSonic systems from space exploration companies, we expect Tekna to see 25%+ annual revenue growth over the next 5 years with EBITDA margins approaching 20%. These robust catalysts drive our bullish stance on Tekna shares.

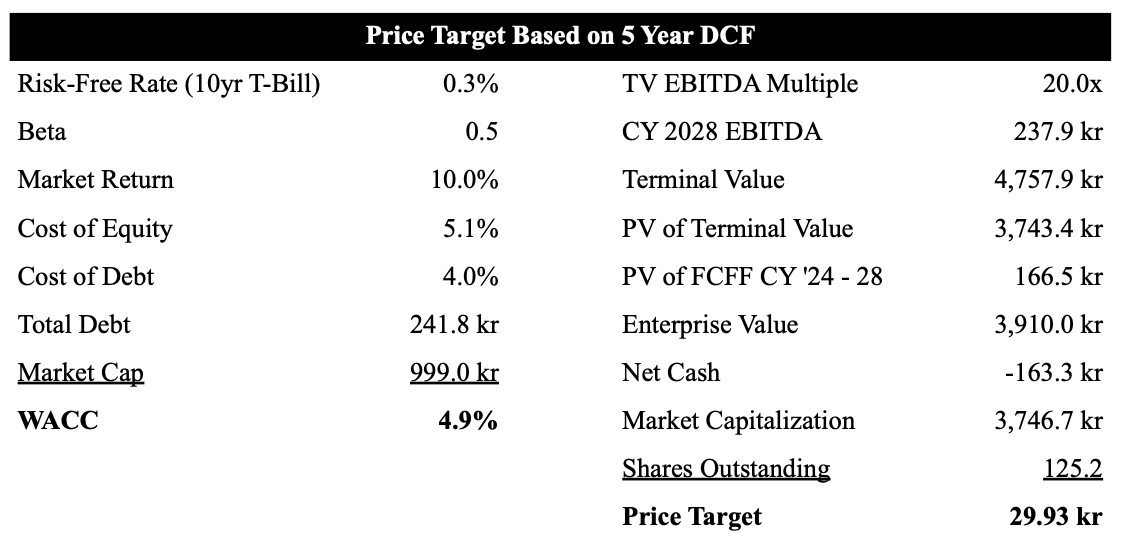

As shown in our table below we use a 5-year DCF model to value Tekna shares. We also value shares in Norwegian Krone (NOK) given they are sold on the Oslo Exchange. Based on our current forecast we value Tekna at 29.93 NOK, which equates to ~400%+ upside at current levels.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.