While Materialise Continues To Trade At Historic LOW Valuation, 1Q24 Revenues and Profits Exceed Expectations - STRONG BUY

While Materialise Continues To Trade At Historic LOW Valuation, 1Q24 Revenues and Profits Exceed Expectations - STRONG BUY

Materialise MTLS 0.00%↑ reported upbeat Q1 results with revenues and profits exceeding consensus expectations. While Q1 revenues were down -3.4% Y/Y, the company acknowledged revenues in 1Q23 were positively impacted by multiple one time revenue items creating a tougher Y/Y comp. Despite lower revenues, MTLS showed strong cost controls in the quarter, reporting stronger than expected profits and cash flows in Q1. Materialise also highlighted the fundamentals across all 3 segments remains strong and reiterated 2024 guidance.

Shares traded down modestly on the results, but on very low volume and on the day the overall market traded down 1%+. Materialise is currently trading at an all-time low valuation despite their ability to continue to grow in a tough macro environment. We believe Materialise shares have meaningful upside over the next 12+ months and remain STRONG buyers.

Key Results vs Consensus Expectations

1Q24 Results

Revenue €63.6M BEAT consensus €62.9M

EBIT €2.7M BEAT consensus €0.1M

EPS €0.06 BEAT consensus (€0.01)

2024 Guidance

Revenue €265-275M (unchanged) vs consensus €270.5M

EBIT €11.0 - 14.0M (unchanged) vs consensus €10.3M

Key 1Q24 Earnings Takeaways

Materialise reported 1Q24 revenues of €63.6M, which was down 3.4% Y/Y. Materialise acknowledged Y/Y growth was impacted by multiple one-time revenue items in 1Q23 creating a tougher Y/Y comp. Growth in the quarter was driven by the company’s Medical segment with revenues up 7.7% Y/Y to €26.2M. Medical software and device sales were up 6% and 9% Y/Y, respectively. MTLS highlighted they have expanded their medical offering into Trauma in the US, and we expect these new applications to be a robust long-term catalyst. Manufacturing revenues were down 10.6% Y/Y to €26.2M as a slow down in prototyping demand impacted sales. However, we are encouraged with the modest Q/Q growth as we believe the European manufacturing landscape continues to improve from mid-2023 lows. Meanwhile the Software segment was down 8.0% Y/Y driven by non-recurring software sales that were down 31% Y/Y as they continue to shift to their recurring CO-AM cloud offering.

Despite lower revenues, Materialise saw strong gross margin expansion in 1Q24 with gross margins growing 60 bps Y/Y to 56.5%. Due to strong cost controls Materialise produced adjusted EBIT of €2.7M, which was better than consensus expectations of €0.1M. Adjusted EBITDA in the quarter was €8.1M, down 21.5% Y/Y largely a result of lower revenue. Medical adjusted EBITDA margins remain strong at 30.3% in the quarter. Software adjusted EBITDA margins of 10.4%, were down from 21.4% in 1Q23 as a result of continued investments and lower revenues. Meanwhile, Manufacturing adjusted EBITDA margins of 5.7% were pressured as a result of lower revenue. Stronger than expected profitability drove robust cash flow in the quarter, with the company generating €10.0M in cash from operations and €8.1M in free cash flow. While Materialise expects accelerated capex investments in Q2 and Q3 as a part of their planned ACTech expansion, we believe the company will continue to produce positive free cash flow for the year.

Materialise reiterated full year 2024 guidance and expects revenue to be in the range of €265 - 275M, which implies 5.4% Y/Y growth at the midpoint. While the company highlighted they expected to grow in all 3 business segments, we believe investors remain discouraged as it implies growth in their Medical business to slow from the mid-teen revenue growth experienced over the last two years. The company highlighted they expect lower medical software sales to device manufacturers to weigh on Medical revenues in 2024, but we believe the company is still positioned to see another year of double digit growth in the Medical segment. The uncertain macro environment is also expected to weigh on growth in the company’s Manufacturing segment. Materialise expects 2024 adjusted EBIT in the range of €11-14M, which is up 26.4% Y/Y at the midpoint. That said, keep in mind this is their new CEO’s first year at the helm, and is likely hoping to establish a solid track record of exceeding expectations. In turn, we view this guidance as likely conservative and could see upward revisions throughout the year.

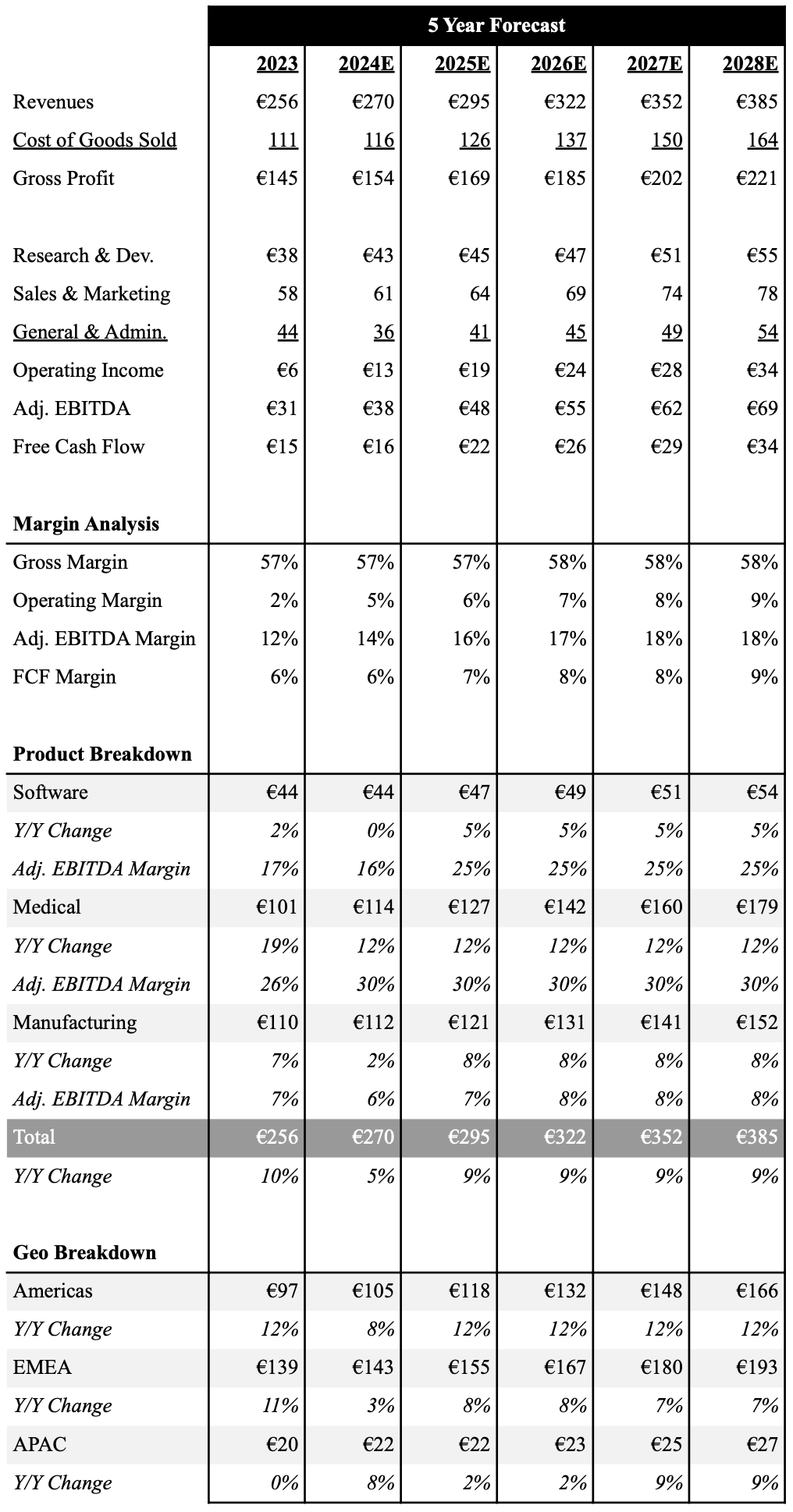

5-Year Financial Outlook

As we highlight below, we are expecting revenues to grow to €270..0M implying 5.4% Y/Y growth. We expect strong execution to allow gross margins to expand modestly in 2024, and operational efficiencies will increase operating margins by 270 bps to 4.5% for the year. We continue to expect Materialise can conservatively grow ~10% Y/Y as macro conditions improve. Coupled with sustained operating leverage, we forecast the company generating mid-teen adjusted EBITDA margins by 2028.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Investment Thesis

Materialise is currently trading at an all-time low valuation despite their ability to continue to grow in a tough macro environment. While weakness in the stock performance has been largely attributed to poor sentiment across the entire additive manufacturing sector, we believe shares have been significantly oversold. Demand for 3D printing patient specific surgical tools and implants continues to rise, and driven by pent up demand for elective surgeries and expansion into new applications we expect the Medical business to continue to see double digit growth for the next several years. Furthermore, the Manufacturing segment has positioned itself as a leading service provider of 3D printed production parts, which we expect to drive high-single digit growth. Lastly, we expect profitability to improve under the company's new CEO. Materialise is currently trading below ~5x EV/EBITDA multiple based on 2025 consensus estimates, which compares to the 5-year average of 40x. These all support our bullish stance and expectation for multiple expansion.

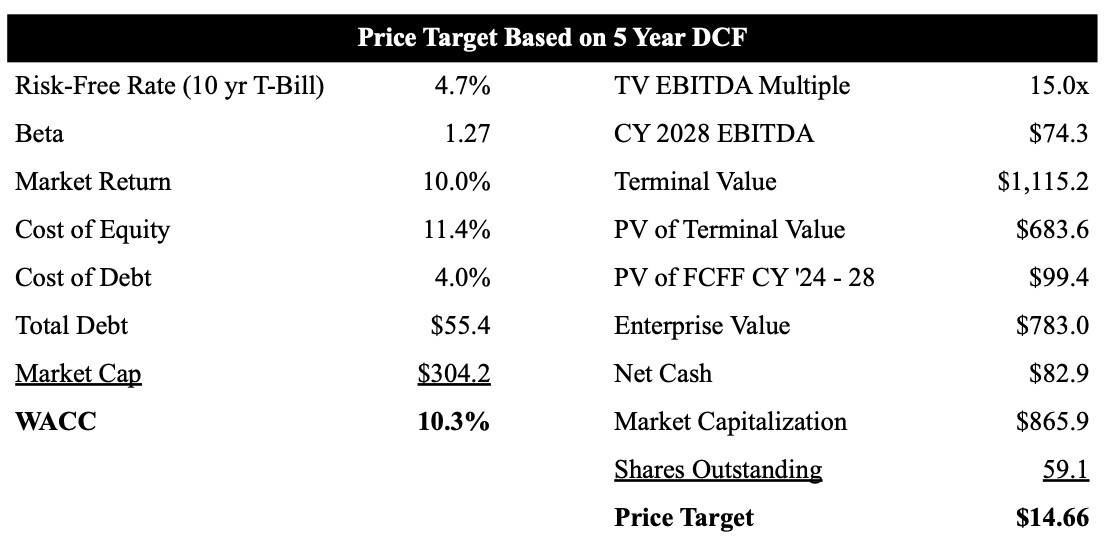

As shown below, we use a 5 year DCF model to value MTLS shares. Based on our current forecast, which we convert into US dollars, and terminal EBITDA multiple of 15x, we value MTLS at $14.66 per share. We raised our price target from ~$12 as a result of slightly lower operating costs as the business grows.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.