Xometry Short Thesis Intact As Company Accelerates Spending and Pushes Out Profitability - SELL

Xometry Short Thesis Intact As Company Accelerates Spending and Pushes Out Profitability - SELL

Xometry XMTR 0.00%↑ announced 1Q24 revenues that exceeded Management and consensus expectations, which we expected based on our 1Q24 pricing analysis. However, higher operating expenditures only translated into adjusted EBITDA loss that was in-line with the Company and analyst estimates. Furthermore, 2Q24 revenue guidance missed modestly, and accelerated international and enterprise investments are expected to drive a higher adjusted EBITDA loss than what analysts were expecting. Shares traded down most of the day on the results, but closed up ~2%.

We continue to applaud Xometry for being able to grow double digits in a challenging manufacturing environment, but we remain cautious on the Company’s revenue outlook with the quick emergence of new marketplace players such as Protolabs. Following 1Q24 results, our bearish thesis remains intact as we believe the Company’s inability to increase revenue per active buyer will force the Company to continue to accelerate spend to grow and underwhelm investors profitability expectations.

Key Results vs Consensus Expectations

1Q24 Results

Revenue $122.7M BEAT consensus $119.9M

Adj. EBITDA ($7.5M) IN-LINE consensus ($7.5M)

2Q24 Guidance

Revenue $127-129M MISS consensus $130.7M

Adj. EBITDA ($6.0)-($8.0M) MISS consensus ($3.8M)

Key 1Q24 Earnings Takeaways

Xometry reported 1Q24 revenues growing 16.5% Y/Y to $122.7M, which was above the Company’s prior guidance ($118 - 120M) and consensus expectations of $119.9M. Revenue in the quarter was driven by Marketplace revenues growing 23.7% Y/Y to $107.2M. Meanwhile, Supplier and Services revenue declined 16.9% Y/Y to $15.5M, which was impacted by discontinuation of the sale of tools and materials. While Xometry saw LTM Active Buyers grow 31.6% Y/Y to 58,504 and added 3,046 new buyers Q/Q, revenue per Active Buyer declined 9.3% Y/Y to $8,218. It is worth highlighting, Protolabs competing Network business grew 39.0% Y/Y in 1Q24 to $23.9M. Furthermore, Protolabs revenue per customer grew ~9% in 2023 to $9,425. We believe Protolabs combination of their Network business and internal manufacturing capabilities makes them a clear leader in the digital manufacturing space.

We were impressed with Xometry’s ability to expand gross margins by 90 bps Q/Q to 39.2%, despite lower revenues as the company’s AI-powered marketplace continues to improve operational efficiencies. Xometry sees gross margins expanding further in 2024. However, the company reported a ~21% Y/Y increase in Sales & Marketing expense that was driven by continued international and enterprise sales personnel expansion. However, we do believe a portion of the increase in S&M is driven by lack of wallet share gains and need to drive new customer growth through paid advertisement. We do not believe this growth strategy is sustainable. Driven by higher opex, Xometry reported 1Q24 adjusted EBITDA loss of $7.5M, which was in-line with expectations. Xomtery is expected to continue this higher investment cycle which will continue to lag profitability, and guided 1Q24 adjusted EBITDA loss of $6-8M, which was much lower than analyst ($3.8M) estimate. We also want to highlight the company moved away from their original commentary where they expect to be adjusted EBITDA positive in Q3 and onward. Rather the Company expects to reach EBITDA profitability when the company hits a run-rate of $600M ($150M per quarter) with gross margin of 38%-40%. The main drivers of the push out are inflationary pressures on items like insurance and employee benefits, as well as necessary business investments. However, we believe the main driver remains limited wallet share expansion among customers.

Xometry is expecting 1Q24 revenues to be between the range of $127-129M, which assumes 15.3% Y/Y growth at the midpoint and in-line with analyst expectations. They continue to expect fiscal 2024 Marketplace revenue growth of at least 20% Y/Y and expect Supplier Services revenue to be down approximately 10% Y/Y driven by the discontinuation of the sale of tools and materials and the wind down of non-core services. This implies mid-teen percent Y/Y growth.

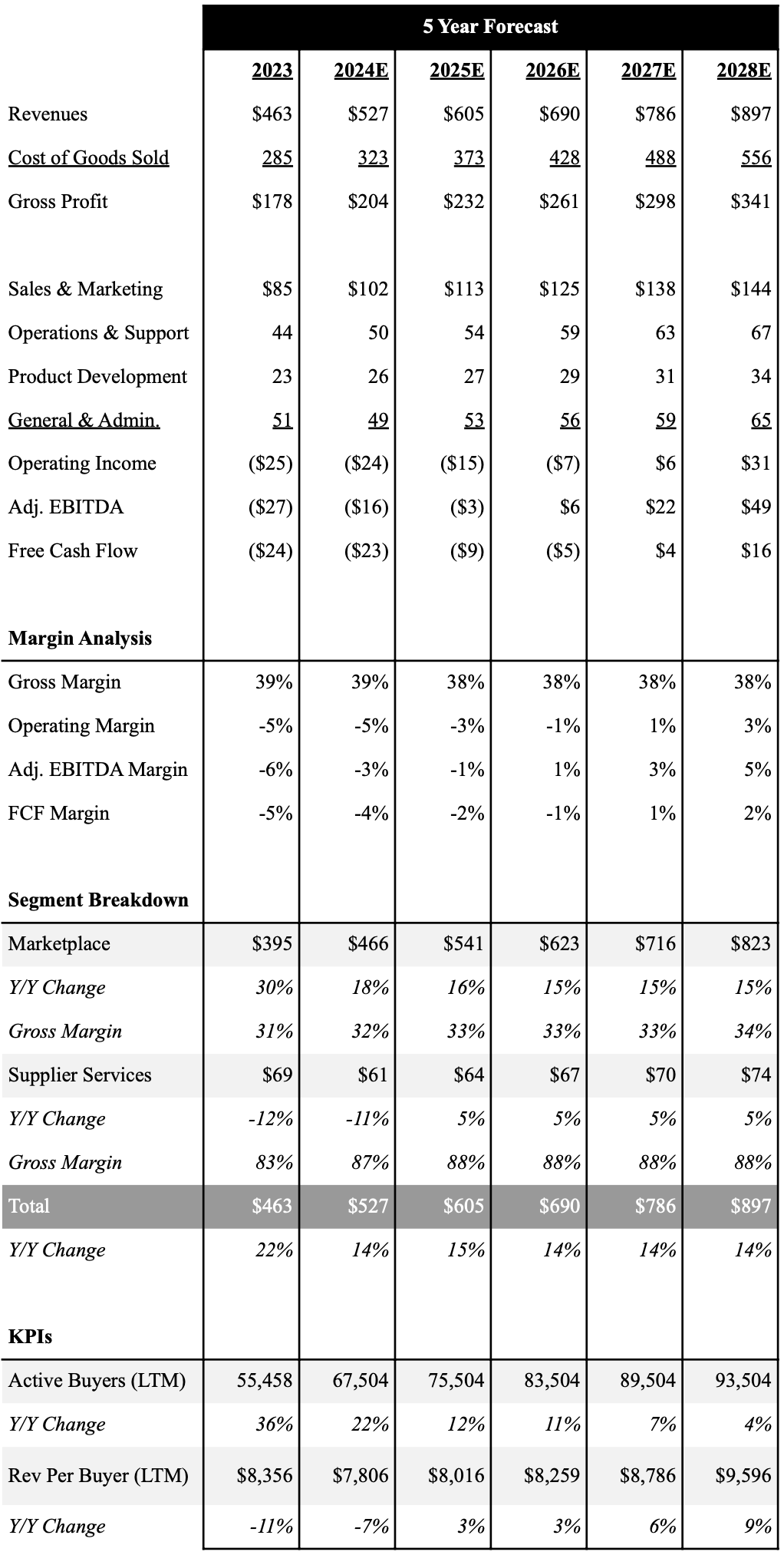

5-Year Financial Outlook

Following 1Q24 results, we have left our revenue estimates mostly unchanged and expect the company to grow revenues 13.7% Y/Y to $526.9M in 2024. Although we believe Xometry can sustain mid-teen revenue growth through 2028, we believe increased competition from the likes of Protolabs will put pressure on Xometry as conditions normalize. In addition, we believe current challenges are beginning to prove out our core thesis and fundamental flaw in the manufacturing marketplace business. When customers need prototypes and low-volume part orders, Xometry is an efficient solution. However, as customers need to go from low to high production part orders it will not make financial sense to pay the 30-40% markup (XMTR gross margin) Xometry charges on their marketplace and rather go directly to the manufacturer. This is why we believe Protolabs internal manufacturing capabilities position them better for long term success. We expect the lack of revenue growth per Active Buyer will pressure profitability, and show the company’s 20 - 30% adjusted EBITDA margin target is a pipe dream. Without a meaningful restructure, we believe mid-single digit EBITDA margins are more likely in 2028.

Below is an overview of our 5 year outlook with a full financial model here.

Source: Industrial Tech Analyst

Investment Thesis

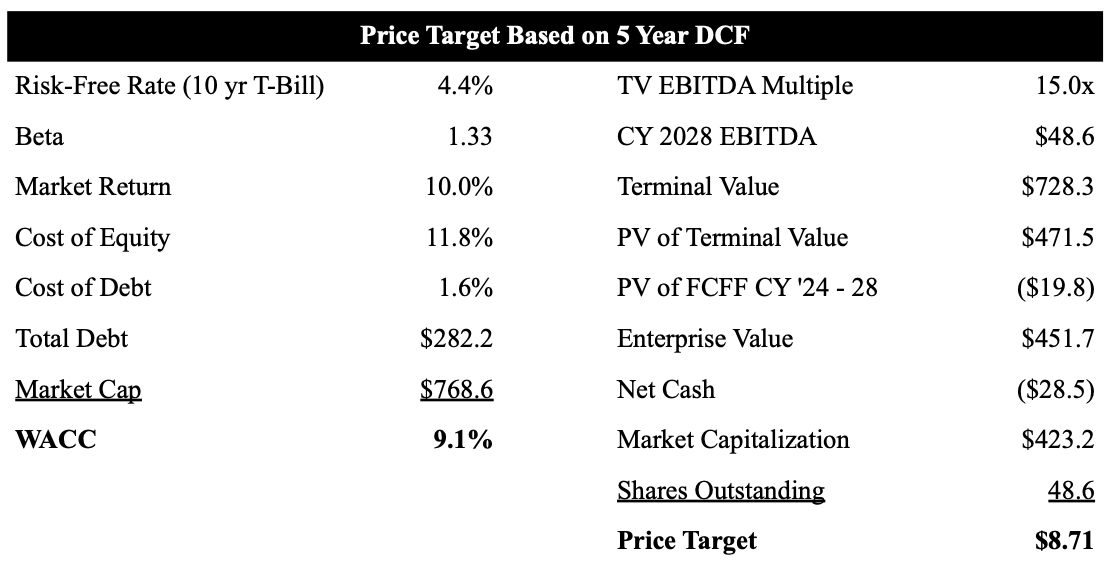

We can not deny that Xometry has been a true disrupter to the digital manufacturing space as their Marketplace revenues have grown from ~$80M in 2019 to ~$395M in 2023, and proven the ability to continue to grow double-digits in a tough manufacturing environment. We do believe Xometry will continue to grow, but are cautious on the company’s revenue outlook with the quick emergence of new marketplace players such as Protolabs and continued challenging macro environment. Furthermore, while we believe Xometry is a great tool to secure prototypes and low-volume production parts, we believe Xometry will struggle to increase wallet share among customers. This coupled with higher opex spend to support new buyer growth, we believe the company will continue to underwhelm investors profitability expectations. These all support our bearish stance and $8.71 price target, which equates to 40%+ downside.

As shown below, we use a 5 year DCF model to value Xometry shares.

Source: Industrial Tech Analyst

Looking to become a better investor or need to find that perfect gift for your finance friend?

Check out these products from our partner Trading Roadmap.

Research Disclaimer: We actively write about companies in which we invest or may invest. From time to time, we may write about companies that are in our portfolio. Content on this site including opinions on specific themes and companies in technology, market estimates, and estimates and commentary regarding publicly traded or private companies is not intended for use in making any investment decisions and provided solely for informational purposes. We hold no obligation to update any of our projections and the content on this site should not be relied upon. We express no warranties about any estimates or opinions we make.